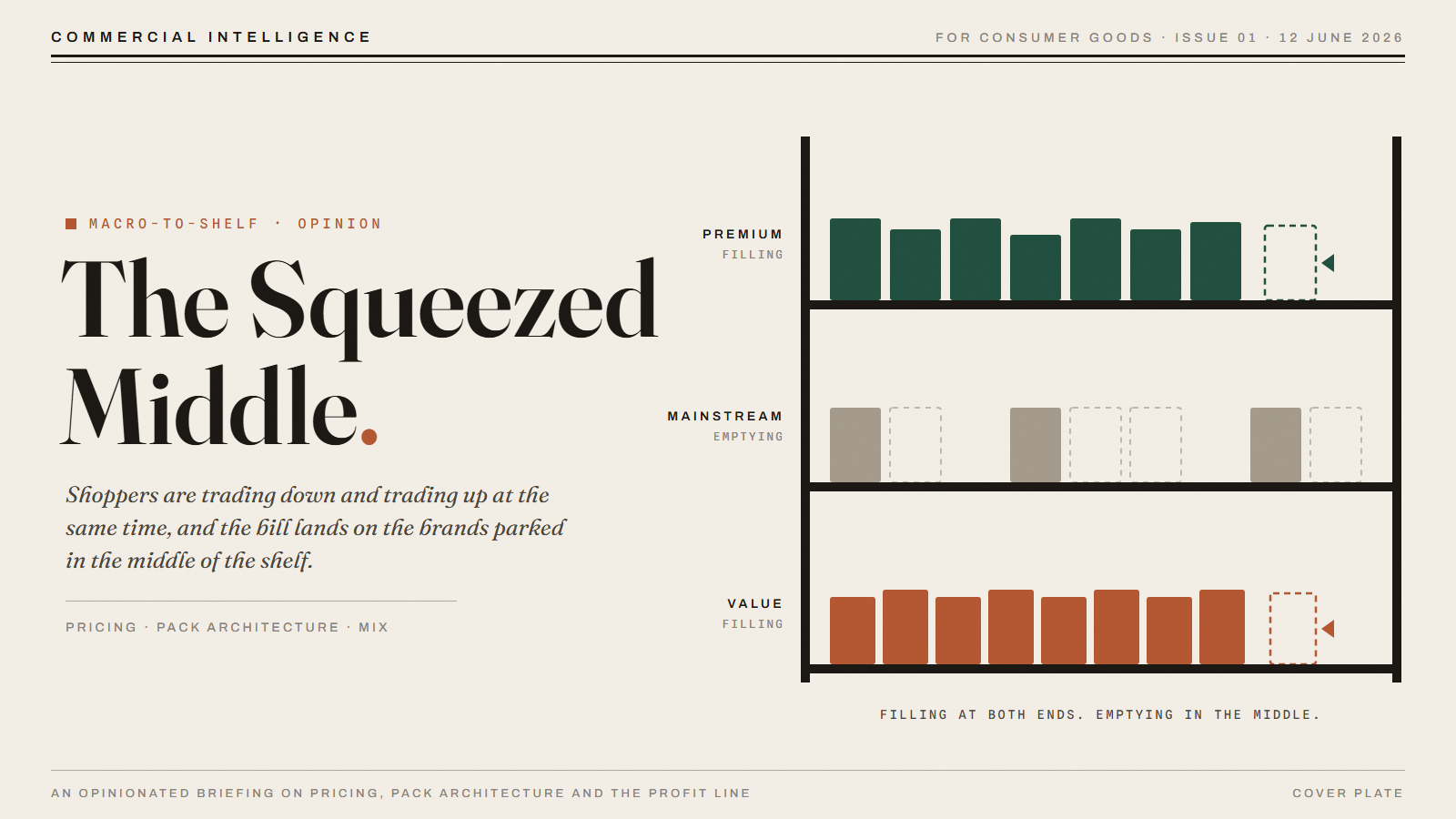

The Squeezed Middle

Shoppers are trading down and trading up at the same time, and the bill lands on the brands parked in the middle of the shelf.

The short version

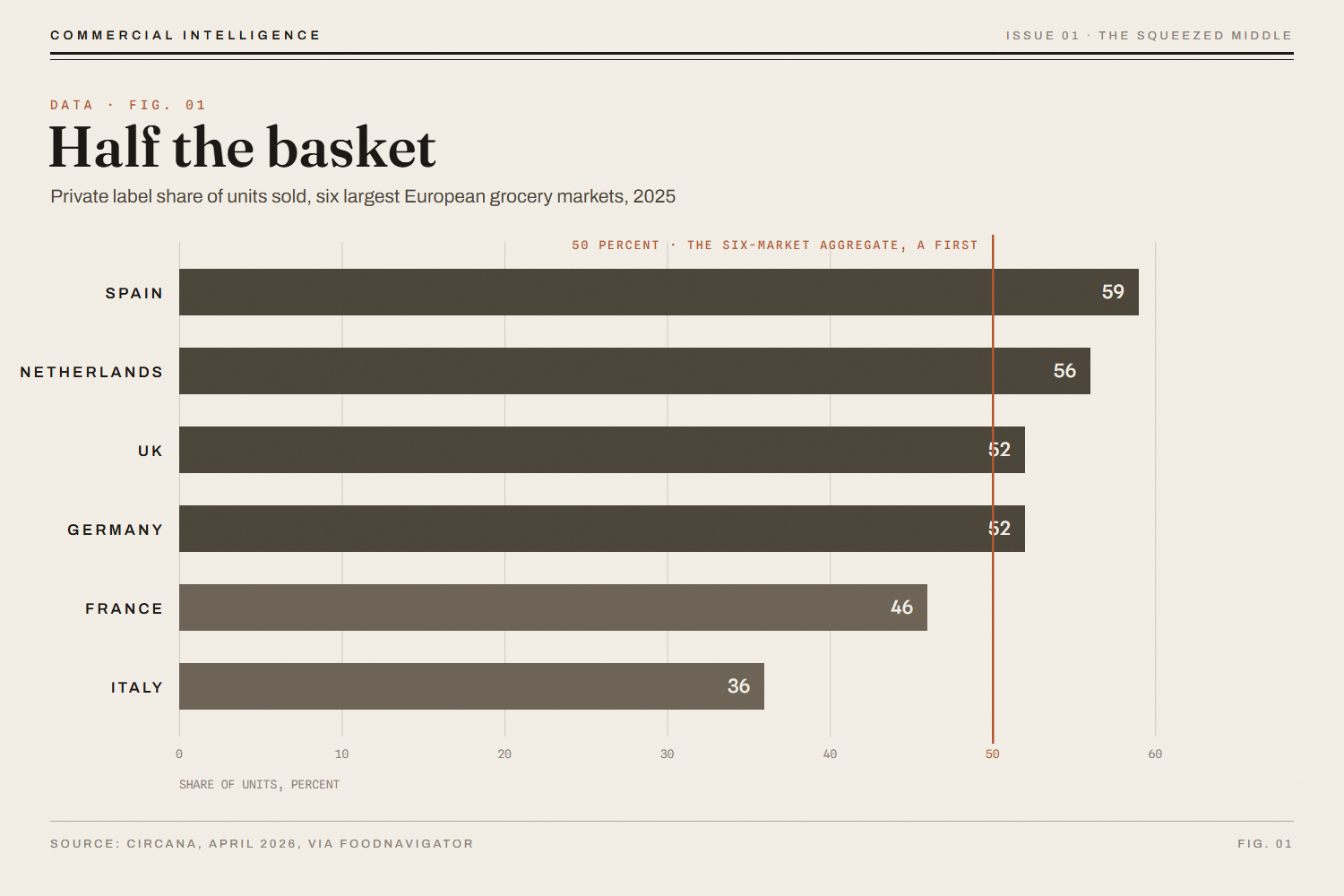

- Private label crossed 50 percent of units sold across Europe's six biggest grocery markets in April, the first time the retailers' own brands have held half the basket (Circana). The same week, McKinsey reported that a majority of European consumers are trading up again.

- Both headlines are true at once because demand is polarising, and the money funding both ends is leaving the same place: the mainstream middle of the shelf, where most established consumer goods portfolios still hold most of their volume.

- I argue the squeeze is structural, not an inflation hangover: private label has gained share for five straight years through every phase of the cycle, discounters hold a far bigger slice of the market than they did in 2019, and 40 percent of American adults now behave as value seekers even though inflation cooled.

- A brand concentrated in the middle loses twice. Shoppers stop compromising toward it once cheaper and better options reset the shelf, and retailers stop protecting its space at the next range review.

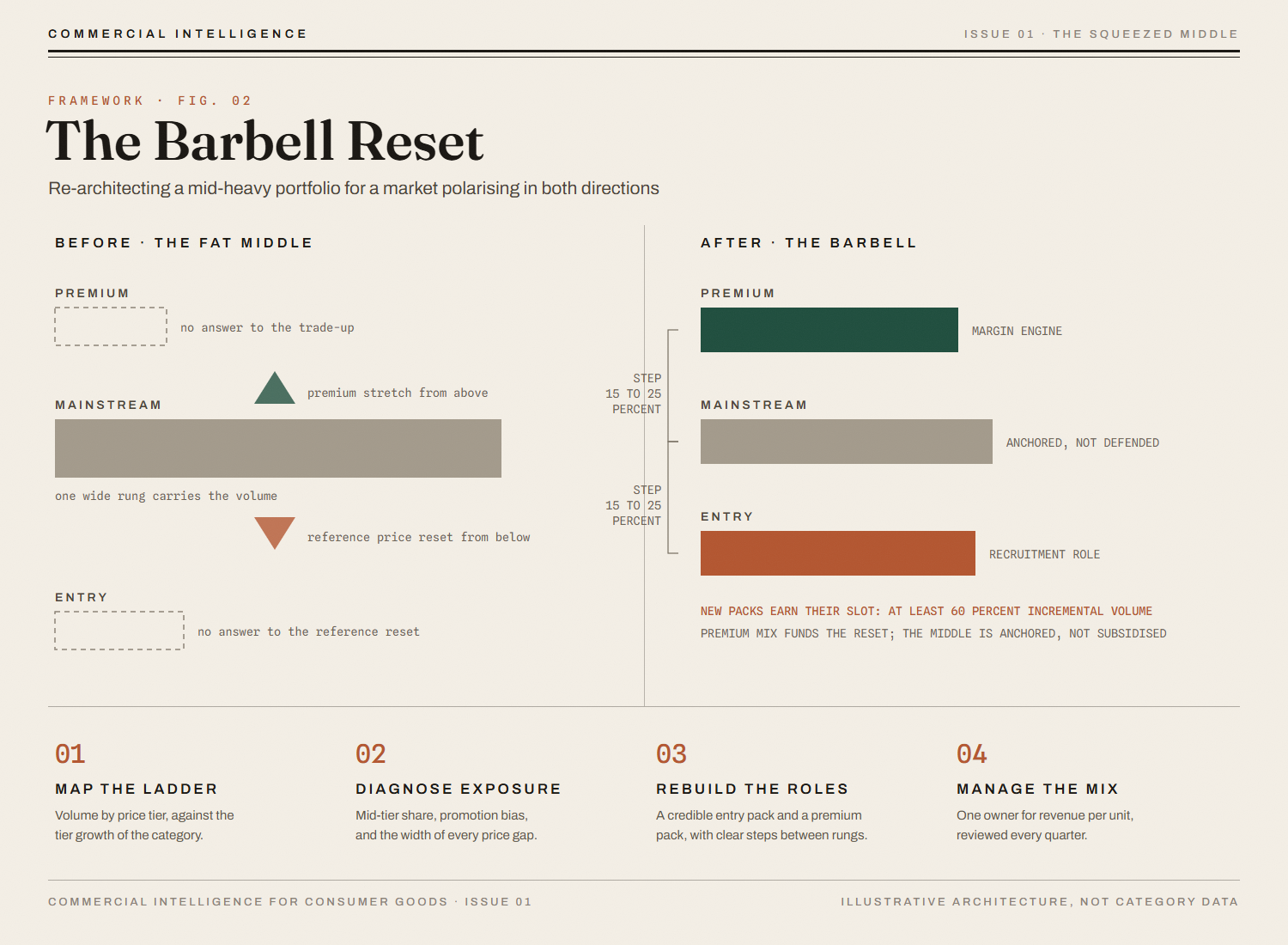

- My position: stop defending the middle with promotion and rebuild the portfolio as a barbell, with a real entry role and a real premium role, anchoring the middle instead of subsidising it.

- In this issue's worked example, the rebuilt portfolio earns 19 percent more gross profit than the one that stands still, while the defend-with-promotion branch is the only one that destroys profit outright.

- And because the blocker is rarely analytical: in most organisations nobody owns the portfolio's architecture, so I'd give one owner the mix line and put tier exposure in front of the board the way you'd put currency exposure there.

Why are shoppers trading down and up at the same time?

Two headlines crossed my desk in the same April week, and at first glance they can't both be true. Circana reported that private label, the retailers' own brands, crossed 50 percent unit share across Europe's six largest grocery markets, the first time own label has held half the units sold (FoodNavigator, 22 April 2026). And in the very same week, McKinsey and EuroCommerce published the State of Grocery Retail Europe 2026 with this as the lead finding: "For the first time in several years, we see a majority of consumers trading up again to higher-quality products," in the words of McKinsey's global head of grocery, Daniel Laubli (EuroCommerce, 21 April 2026).

So which is it, a value market or a premium market? It's both, and that's the story. Part of the polarisation runs between households: stretched families anchoring the value end while better-off shoppers premiumise. But some of it, and every category manager I know sees this in their own data, runs through the same shopper in the same basket. The person who picks up the discounter's pasta without a second thought will pay properly for the olive oil they care about. Shoppers aren't trading down or trading up so much as abandoning the compromise in the middle, in both directions at once.

If you run a brand, the uncomfortable question is where the money for both moves comes from. It comes out of the mainstream middle, that broad band of safe, familiar, mid-priced products where most established portfolios were built and where most of their volume still sits.

Is this just the inflation hangover?

The comfortable reading says shoppers fled to cheap during the 2021 to 2023 price shock and will drift back once wages recover. I'd like that to be true. The evidence keeps refusing it.

Start with how stubborn the trend has been. European private label unit share has now risen for five consecutive years, through 2024's disinflation just as much as through the spikes (Circana). If this were purely a price-shock reflex, 2024 should have bent the curve, and it didn't.

Then look at who the value seekers actually are. Deloitte's June 2025 study, built on more than 900,000 consumer data points, counted 40 percent of American adults as active value seekers, and nearly three in ten of them live in six-figure households. Value seeking looks less like an income band and more like a learned habit: once a shopper finds the cheaper option is good enough, the habit outlives the inflation that taught it.

The supply side has changed shape too. Discounters, the hard-discount grocers whose ranges are mostly own label, now hold 23.2 percent of the European grocery market, up about 2.6 points since 2019 (McKinsey, State of Grocery Retail Europe 2025), and a store estate doesn't un-build itself when inflation eases. More telling still, private label now accounts for 70 percent of new food launches in Western Europe (NielsenIQ). That one stopped me when I first read it. Innovation used to be the brand manufacturer's moat, the thing a retailer's copy could only follow at a distance. In food, the followers are now launching more than the leaders.

And the pressure isn't finished. US grocery prices rose 0.7 percent in April alone, the biggest monthly jump since 2022, while real earnings fell for a second straight month (Purdue, May 2026). The value end of this squeeze has a next leg coming.

How bad does it get in the accounts?

Bad enough that you can read it straight off the income statements.

In the United States, private label grew 3.3 percent in 2025 to a record 282.8 billion dollars while national brands grew 1.2 percent (Retail Dive, January 2026). Nearly three times the growth rate, compounding year after year, eventually shows up in the league table: manufacturers with more than 8 billion dollars in sales lost share for the third consecutive year (Circana 2025 Growth Leaders). My read on why size is the tell: the giants aren't badly run, they're over-exposed. Portfolios of that scale were engineered for the broad mainstream, and the mainstream is the band that's draining in both directions.

Kraft Heinz is the cleanest single example, because the company published the breakdown. Organic sales, which strip out currency swings and acquisitions to show how the underlying business actually traded, fell 3.4 percent in 2025: price contributed plus 0.7 points, and volume and mix took away 4.1 (company release, 11 February 2026). Prices nudged up, and four points of trade walked out anyway. Gross margin fell 140 basis points, which is 1.4 percentage points of profitability gone, and the company wrote 9.3 billion dollars off the value of its brands. An impairment that size is a board formally telling its own investors the portfolio is worth less than it once believed.

Mix, and how to read a results bridge. Companies decompose their growth into price, volume and mix, the bridge you'll see in every results release. Price and volume are obvious. Mix is the quiet one: sell a little more of what earns you more per unit, and revenue and margin improve with no price increase and no extra volume sold. It hides inside averages, which is why most monthly reports miss it, and in my experience it's the line most boards have never been shown.

Nor is this one company's stumble. Across eleven of the largest global players, average organic growth fell from 3.9 percent in 2024 to 1.5 percent in early 2025, with volumes turning negative as a group; Mondelez grew value 6.6 percent while its volume fell 3.5 percent (Sevendots, May 2025). The sector has spent three years pricing over a shrinking volume base, and that trick has a floor. Why? Because every round of pricing widens the gap to the shopper's reference price and to the own label sitting next to you, so the volume response gets a little worse each time. And because factories, warehouses and trucks are full of fixed costs, every point of lost volume makes the remaining units dearer to produce. Price up, volume down, unit costs up: that's how a company can raise prices and still watch its gross margin fall.

Why does the middle break first?

To see the mechanics, you need one idea from pack price architecture (PPA), which is the discipline of designing your range of pack sizes and price points as one system rather than one pack at a time. Picture your category as a ladder with three rungs. The entry rung wins on the cash the shopper hands over at the till. The premium rung wins on a clear answer to "what am I paying more for?". And the mainstream rung in between wins on something quieter: it's the safe choice, the one that needs no decision at all.

Why the middle option usually wins. Put three options in front of a shopper and most will avoid the extremes. Choosing the middle feels prudent: not the cheapest, not the most expensive, nothing to justify to yourself or anyone else. Behavioural economists call this the compromise effect. In well-built three-tier ranges, the middle option captures roughly half of all choices, sometimes more. The middle of a ladder is valuable real estate, for exactly as long as it's genuinely perceived to be the middle.

That last clause is the trap, because the effect works on the options the shopper sees, not on your price list. When private label and discounters move in below you, they reset the reference price for the whole category, and your mainstream pack stops being the middle without moving an inch.

Reference price, in plain words. Every shopper carries a rough memory of what a product should cost, built from what they paid and saw recently. Prices above that internal benchmark feel like losses, and losses sting roughly twice as hard as equivalent savings please. So when a 1.49 own label sits next to your 2.29, the shopper's benchmark drifts down, and your unchanged price starts to feel expensive without you touching it.

The same thing then happens from above. Retailers have pushed their own premium ranges hard, so the top of the ladder stretches away from you as well. Your pack hasn't moved, but everything around it has, and a shelf position is always relative. The brand that used to be the sensible middle is now read as the expensive version of cheap by one shopper and the basic version of good by the next.

What do most brands do about it? They rent the volume back. Across those six European markets, 34 percent of branded units sold on promotion, against 14 percent for private label (Circana). I've watched this cycle play out enough times to know how it ends, and the arithmetic is unforgiving: of the extra volume a deep deal generates, only about a third tends to be truly new, while the rest is your own shoppers switching between your own packs and loading their pantries at the discounted price. Run that calendar for a few years and you've trained your most loyal buyers to wait for the deal, eroded your everyday baseline, and worsened your mix.

Meanwhile the retailer is doing its own maths, and you should assume it's doing that maths well. Grocery margins are thin and getting thinner: the big European grocers' operating overheads climbed from 19.0 to 19.7 percent of revenue between 2022 and 2025 (McKinsey and EuroCommerce), so every metre of shelf is under more pressure to pay rent. The retailer's own label delivers margin with no negotiation attached, while a mid-tier brand with heavy trade funding and softening velocity, the rate at which it sells per store, is occupying space the retailer could monetise better. And the terms structures cut the same way: in the trade agreements I've seen, the discounts and the shelf programmes scale with the breadth of range a supplier brings, so a brand offering entry, mainstream and premium roles negotiates a visibly better deal than a brand offering one crowded rung, before the conversation even turns to price. A mid-only brand walks into every range review holding the weakest hand at the table. That's how a squeezed brand ends up a delisted one.

Defending the middle is the wrong fight

Every instinct says defend: hold the price point, deepen the deals, relaunch the hero pack. I think that's the wrong fight. It's a cyclical answer to a structural problem, and it spends your margin subsidising a tier that demand is leaving.

The better position is to rebuild the portfolio as a barbell. At one end, a real entry role: a pack that competes on cash outlay for the value-seeking shopper without wrecking your economics. The craft is that a good entry pack is usually cheaper to buy and dearer per kilo. You protect margin through pack size, not through list price cuts, and the shopper still gets what they came for, which is a smaller number at the till. At the other end, a premium role: a pack that gives your trade-up shopper somewhere to land inside your brand. And premium needs a visible reason, not just a higher number: a better format, an upgraded recipe, an occasion the mainstream pack doesn't serve, the weekend version, the gifting version, the single-serve indulgence. The cue has to survive three seconds at the shelf. Premiumise the experience, not just the price; a 25 percent premium with nothing visible behind it is a price rise wearing a costume.

Fair question at this point: why would a retailer give you that entry slot at all, when the value rung is its own margin engine? Two reasons, and both are about the retailer's own war. A supermarket's most dangerous competitor isn't the brand next to you on its shelf, it's the discounter across the road, and a branded pack at an entry price helps the grocer give its price-anxious shoppers one less reason to make that trip. And range breadth is currency in the terms negotiation, as we saw a moment ago: the supplier who brings a working ladder is worth more to the category line than the supplier defending one rung. Your entry pack doesn't have to beat own label on price. Its job is to stop your own shoppers walking out of the brand, and to make the rest of your ladder look fairly priced on the way past.

The middle doesn't vanish in this design. It narrows, and it ends up belonging to the brands that anchor it on purpose rather than defend it out of habit. If more than half your volume sits mid-tier with nothing credible at either end, you don't own the mainstream; you're exposed to it.

What would make me wrong? If real wages recover and the trade-up McKinsey describes broadens into mainstream brands rather than past them, the middle regains its anchor and defence becomes viable again. It could happen. But with own label gaining share for five straight years through every phase of the cycle, I wouldn't bet a portfolio on it.

What does the fix look like in numbers?

Take an invented brand with deliberately simple numbers. They're made up, but they add up, and you can recompute every figure yourself.

The brand sells 100 units of one mainstream pack at 1.00 per unit on a 33 percent gross margin: 100.00 of revenue, 33.00 of gross profit. Its tier now sheds a tenth of its volume to the two ends, which is the polarisation we've been describing. Do nothing, and the brand follows its rung down: 90 units, 90.00 of revenue, 29.70 of gross profit.

Suppose instead you defend, the instinct from the last section: you hold all 100 units by promoting, with 33 of them selling at 25 percent off. Revenue comes to 91.75 (67 units at full price, 33 at 0.75), and with costs unchanged at 0.67 a unit, gross profit lands at 24.75. That's below even the do-nothing case's 29.70, and it's before the deals train your shoppers to wait for the next one. Defending the middle with promotion is the only branch in this example that destroys profit outright.

Now re-architect instead. Add an entry pack at 0.85 with a 26 percent margin, recruiting 8 units of value-seeking demand. Add a premium pack at 1.25 with a 44 percent margin, capturing 7 units of trade-up. Those 15 new units are more than the 10 that left the tier, and that's the point of the new roles: they don't just catch your leavers, they recruit from competitors' packs at the two ends. The portfolio now sells 105 units for 105.55 of revenue and 35.32 of gross profit, a 33.5 percent blended margin, the weighted average across everything it now sells. Against standing still, that's 17 percent more revenue and 19 percent more gross profit, and the overall margin rises even though the entry pack dilutes it, because the premium mix more than pays for the dilution. None of these margins is exotic. In the pricing playbooks I work with, a healthy three-tier ladder typically runs in the mid twenties at entry, the mid thirties in the middle, and forty plus at the top, and the premium tier often earns several times the profit per unit of the value tier.

Two disciplines keep the example real outside a spreadsheet. First, the rungs need daylight: price steps of roughly 15 to 25 percent between tiers. Any tighter and the shopper can't tell your tiers apart, so the architecture collapses back into one blurred offer. Much wider and you've left a hole on the shelf, and holes on shelves get filled, usually by an own label. Second, every new pack has to earn its slot. The gate I use is incrementality: if much less than 60 percent of a new pack's volume is new money, rather than shoppers shuffled across from your existing packs, the pack is eating your core rather than extending it. And the example survives its own gate: even if only 60 percent of those 15 new units are incremental and the other six cannibalise the mainstream pack, the rebuilt portfolio still earns about 33.34 of gross profit, roughly 12 percent ahead of standing still.

Once the architecture is in place, manage mix as a number with an owner. Disciplined mix programmes, which steadily shift weight toward the packs and channels that earn more per unit, are typically worth between half a point and a point and a half of revenue per unit each year. In this margin environment, that's the difference between a flat year and a good one.

Why does nobody own this fix?

Because in most organisations, nobody owns it. Marketing owns the brand ladder, sales owns the terms and the promotion calendar, supply owns which pack formats exist, and finance reports price and volume but rarely mix. Every function touches the portfolio's architecture, and no one is accountable for it. So promotion drifts toward the biggest mid-tier pack, because that's where uplift is easiest to buy, and the entry and premium launches die in business cases built on cannibalisation fears that nobody has actually measured.

The fix is organisational before any analysis helps: give one owner the mix line, revenue per unit across the portfolio, and have them review it quarterly with the same seriousness as the annual price increase. Where that owner sits matters less than that the role exists with teeth: a revenue growth management head where you have one, otherwise finance with a commercial mandate. Make promotional approval depend on mix effect, not just on uplift. And put tier exposure in front of the board the way you'd put currency exposure in front of them: as a position the company holds, with a number attached, not as a marketing detail.

What would I do on Monday?

If this were my portfolio, I'd make three moves, in this order. First, I'd map the volume by price tier against the tier growth of the categories, and if more than half of it sits mainstream, I'd say that number out loud in the next planning cycle, because naming the exposure is what unlocks the budget to fix it. Second, repair the ladder: a credible entry role, a credible premium role, clear price steps between the rungs, and pack economics that reward the shopper for climbing. Third, re-bias the promotional calendar away from the middle, and start measuring mix every quarter so you can watch the architecture pay back.

The middle of the shelf was a wonderful place to build a consumer goods business for half a century, while it was wide. It's narrowing from both sides now, and it will keep narrowing whether or not your portfolio is ready. If it were mine, I'd start building the ends while the middle can still pay for the work.

Signals

Five data points worth your time this week.

- Private label crossed 50 percent unit share across Europe's six largest grocery markets, from 59 percent in Spain to 36 percent in Italy (Circana, April 2026). https://www.foodnavigator.com/Article/2026/04/22/how-food-and-drink-brands-can-beat-private-label/

- McKinsey and EuroCommerce describe a polarised recovery: a majority of European consumers trading up while grocery volumes are projected to crawl at 0.2 percent a year through 2030. https://www.eurocommerce.eu/2026/04/european-grocery-retail-models-are-in-motion-while-margins-remain-under-pressure/

- Kraft Heinz closed FY2025 with volume and mix down 4.1 points and 9.3 billion dollars of impairments. https://news.kraftheinzcompany.com/press-releases-details/2026/Kraft-Heinz-Reports-Fourth-Quarter-and-Full-Year-2025-Results/default.aspx

- US private label hit a record 282.8 billion dollars in 2025, growing almost three times as fast as national brands. https://www.retaildive.com/news/retail-private-label-record-sales-volume-2025/810390/

- US food-at-home prices rose 0.7 percent in April, the largest monthly jump since 2022, with real earnings down two months running. https://ag.purdue.edu/commercialag/home/paer-article/the-april-2026-cpi-and-ppi-reports-the-food-price-pipeline-is-opening-purchasing-power-under-pressure-for-second-consecutive-month/

Sources

- Circana private label release (April 20, 2026), via FoodNavigator (April 22, 2026): https://www.foodnavigator.com/Article/2026/04/22/how-food-and-drink-brands-can-beat-private-label/

- McKinsey and EuroCommerce, State of Grocery Retail Europe 2026, press release (April 21, 2026): https://www.eurocommerce.eu/2026/04/european-grocery-retail-models-are-in-motion-while-margins-remain-under-pressure/

- Retail Dive on PLMA and Circana Unify+ US private label data (January 26, 2026): https://www.retaildive.com/news/retail-private-label-record-sales-volume-2025/810390/

- Kraft Heinz fourth quarter and full year 2025 results (February 11, 2026): https://news.kraftheinzcompany.com/press-releases-details/2026/Kraft-Heinz-Reports-Fourth-Quarter-and-Full-Year-2025-Results/default.aspx

- Sevendots, the volume challenge across 11 large CPG companies (May 19, 2025): https://sevendots.com/for-large-cpg-companies-the-volume-challenge-is-increasingly-obvious/

- Purdue Center for Commercial Agriculture, April 2026 CPI analysis (May 18, 2026): https://ag.purdue.edu/commercialag/home/paer-article/the-april-2026-cpi-and-ppi-reports-the-food-price-pipeline-is-opening-purchasing-power-under-pressure-for-second-consecutive-month/

- Deloitte Consumer Industry Center, the value-seeking consumer (June 2025), and Circana 2025 CPG Growth Leaders (14th annual): cited by name; figures verified against the knowledge-base digests of the underlying reports.

- Method material (tier roles, compromise effect, reference price, promotion decomposition, mix benchmarks, terms breadth): the Commercial Intelligence knowledge base, taught as practitioner method; benchmark ranges stated as typical ranges.