Retail Media: Trade Spend in a Better Suit

Retail media is the trade money you always paid, in a better suit. Govern it like the trade investment it is, before the next plan.

The short version

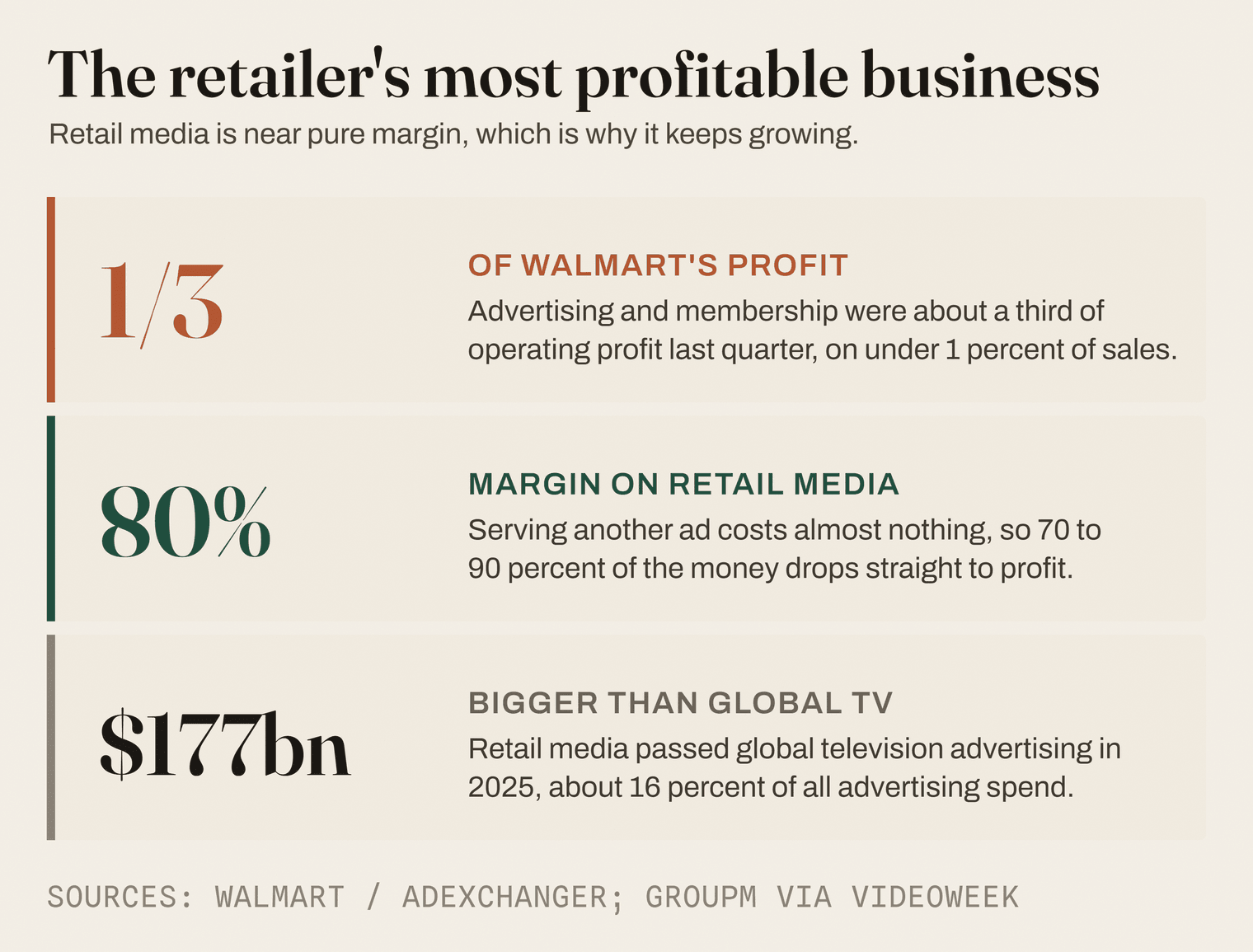

- Retail media just passed global television advertising and has become the retailer's most profitable business. About a third of Walmart's most recent quarterly operating profit came from advertising and membership, on an advertising line that is less than one percent of its revenue [1].

- That profit is near pure margin, somewhere between 70 and 90 percent, which is exactly why retailers push it so hard and why it grows inside your joint business plan every single year.

- It is not new money. It is the trade and customer marketing money that has always flowed from your profit and loss to your retailer's, repriced at a higher margin and handed to a part of your organisation that does not run it through a return-on-investment gate.

- The return on ad spend on your dashboard is not the same thing as incrementality. Most of the sales it claims you would have made anyway, which is the precise mistake this industry already made, and paid for, with trade promotion.

- My position: govern retail media as trade investment. Put one owner on it, set an incrementality hurdle before you commit, demand a holdout test, and consolidate onto one measurement spine, before you sign the next plan.

- The good news hiding in the bad news: your retailer now needs your advertising money more than your product margin. That is leverage, not just a bill. Most brands are not using it.

A third of Walmart's profit is now advertising. Whose budget do you think paid for it?

Walmart told investors something this year that should stop a commercial director mid-sentence: advertising and membership income together made up roughly a third of its operating profit in the quarter, and its global advertising business reached about 6.4 billion dollars, up 46 percent on the year before [1]. The largest retailer on earth, a company built on moving pallets of groceries at razor-thin margins, now leans on advertising for a third of the profit it reports to Wall Street.

And that advertising money came, in large part, from you. From the consumer goods brands that spend to be seen on its website, its app, and increasingly its in-store screens. The money you used to call shopper marketing, or trade, or digital, has quietly become the most valuable product your retailer sells. It is not selling more cereal. It is selling access to the people already walking down the cereal aisle, and it is selling that access back to the brand that put the cereal there.

This is the story of how the oldest money in the trade relationship put on a media plan, learned to call itself advertising, and slipped out of the one discipline you would normally apply to it. It is also the story of how to get it back under control, because the tools you need are already in your building. You use them on trade promotion every week.

What is retail media really, and how did it just pass television?

Let me define the thing plainly, because the jargon does a lot of work to make it sound newer than it is. A retail media network, which I will call an RMN from here, is the advertising business a retailer runs using its own shopper data. When you pay Amazon to put your product at the top of a search for "coffee," that is retail media. When Tesco or Kroger uses what it knows about its loyalty shoppers to show your ad somewhere else on the open web, that is also retail media. The retailer owns the shopper relationship, the purchase data, and the screen, and it rents all three back to you.

The scale is the part that has changed. Retail media overtook global television advertising in 2025, reaching roughly 177 billion dollars worldwide, about 16 percent of all advertising spend on the planet [2]. It is now the fastest growing major channel in advertising, expanding at around 14 percent a year while older channels crawl [3]. In the United States alone, brands spent somewhere around 60 billion dollars on it in 2025, heading toward 70 billion in 2026 [4]. Amazon by itself took in about 68 billion dollars in advertising last year [5], and accounts for roughly three quarters of all US retail media [4].

What counts as off-site retail media? On-site is the easy bit: ads on the retailer's own shop, like sponsored search and product placements. Off-site is where the retailer takes what it knows about its shoppers and uses it to target them somewhere else, on the open web, on social, or on streaming television, then matches the resulting sales back to its own till data. Off-site is growing about twice as fast as on-site, because verified "these people actually bought the category" data is worth more than the guesswork most advertising runs on [4]. It is also harder to check, which matters later.

You do not need to carry these numbers in your head, but you do need to register the direction. A line of spend that did not have a name a decade ago is now bigger than television and growing faster than anything else in marketing. When something moves that fast, it usually means the money is being repriced, and someone is capturing the difference.

Why has your retailer suddenly fallen in love with selling you ads?

Because the margins are extraordinary, and because the rest of the business is so hard.

A grocery retailer keeps something like 3 to 7 pence of net profit on every pound that goes through the till. That is a brutal way to make a living, and it is why supermarkets behave the way they do on price. Retail media does not work like that. Once the retailer has built the technology and bought the data team, the cost of showing one more ad is almost nothing, so the margin on advertising revenue runs somewhere between 70 and 90 percent. That is why a business that is a rounding error on the top line can become a third of the profit. Marketplace Pulse put it bluntly: without its high margin advertising, Amazon's retail business "would be increasingly unprofitable" [6]. Advertising is not a side hustle for these companies. It is increasingly the point.

Kroger, a grocer, made about 1.35 billion dollars of operating profit from what it calls its alternative profit businesses, led by its media arm, with media income up 17 percent [7]. Read the language. A supermarket now has a profit centre that has nothing to do with selling food, and it is growing far faster than the food.

So when your account team sits across the table and the retailer is unusually enthusiastic about a media package, understand what is happening. You are not being offered a marketing opportunity. You are being invited to fund the most profitable, fastest growing part of your customer's business. They are not wrong to ask. The question is whether you are right to say yes on the terms offered, and most brands are saying yes without doing the sum. Part of why that yes comes so easily is that the scorecard you use to judge the spend is the retailer's own, and it is built to look generous. That is the next problem.

Haven't you paid this bill before?

You have. This is the part the word "media" is designed to make you forget.

Money has always flowed from a manufacturer to a retailer beyond the simple price of goods. You pay to get listed. You pay for the promotion. You fund the loyalty card, the leaflet, the end-of-aisle display, the "customer marketing" line that finance never quite loved. This is back margin, the trade's name for the income a retailer earns from you outside the shelf price. Total gross margin on a mainstream branded grocery line tends to run around 25 to 35 percent, and in heavily promoted categories the back margin, the part you fund through deals and fees, can be 60 percent or more of it. The shelf price you can see is often the smaller half of the deal.

Retail media is the newest, glossiest entry in that ledger, the same back margin given a dashboard and a media plan. The customer marketing fund that used to buy a feature in the loyalty mailer now buys a sponsored search slot, and the invoice is bigger. Around 47 percent of brands already fund their retail media through joint-business-plan co-op money, the same pot that funds trade [8]. The spend did not appear from nowhere. It was reclassified, repriced, and rebadged.

The gross-to-net waterfall, and where retail media lands Every brand has a waterfall between the price on the invoice and the money it actually keeps. You start with the list price, then subtract the on-invoice discounts, the off-invoice rebates, the promotional funding, and the customer marketing money. What survives at the bottom is your net sales, the figure your profit and loss actually runs on. For a typical consumer goods company, the gap from top to bottom is large; trade investment alone often runs 15 to 20 percent of gross sales, and a good deal more in over-promoted categories. Retail media is a new step in that waterfall. The danger is that it is being added at the top, as fresh "media" spend, while behaving like another deduction at the bottom. If you do not place it in the waterfall, you will double-count it as growth investment when it is really a cost of selling.

I am not saying retail media is worthless. Targeted, measured, and aimed at genuinely new shoppers, it can be some of the most efficient money you spend. I am saying that calling it media, and routing it through the marketing team, stripped it of the scrutiny you apply to every other pound that crosses to the retailer. You would never let a trade term grow 40 percent a year without asking what it bought. Retail media has been getting exactly that free pass.

Does any of it actually sell anything more?

This is the question the whole thing turns on, and it has an uncomfortable answer.

The metric your retailer reports is return on ad spend, or ROAS, the sales attributed to an ad divided by what the ad cost. A ROAS of four sounds like four pounds back for every pound in. The trouble is that ROAS counts every sale the ad touched, including all the sales you were going to make anyway. A shopper who already wanted your coffee, searched for it, clicked the sponsored result at the top, and bought it, looks identical in the data to a shopper the ad genuinely won. The first one is not incremental. You paid to be shown to your own customer on her way to the till.

Incrementality is the only number that matters: the extra sales you would not have made without the spend. And here the industry is repeating, almost line for line, the most expensive lesson of trade promotion. The pattern that trade-promotion analysis keeps returning to is sobering: only about a third of the volume a deal appears to create is genuinely incremental, and a large share of promotions never earn back their cost. We learned that the hard way, with years of "successful" promotions that were quietly destroying value. Retail media is walking the same path, and the people grading the test are the same people selling it.

That is not my characterisation, it is the industry's own. As one analysis in The Drum put it, ROAS "became the metric that was achievable, relatively easy to calculate, and within the retailer's control" [9]. Proving real incrementality is now the single most cited barrier to retail media investment, named by about a third of senior leaders, and only around 56 percent of brands rate their own measurement as strong [8]. Worse, there is no shared definition of what incremental even means; ask three brands and you will get three answers. When the seller controls the scoreboard and the buyer cannot agree on the rules, the number on the screen is marketing for the network, not management information for you.

ROAS, incrementality, and the holdout test ROAS asks: of the sales linked to this ad, how much money came back? Incrementality asks the harder question: how many of those sales would not have happened without the ad? The gap between them is the sales you paid to reach people who were already buying. The clean way to tell them apart is a holdout test: hold a comparable group of stores or shoppers out of the campaign, run the ad to everyone else, and measure the difference. The lift over the held-out group is the real number. If a network cannot or will not support a holdout, treat its ROAS as a brochure, not a measurement.

What does it do to your profit and loss, and to theirs?

Let me put numbers on it, because the abstract version lets everyone off the hook. The following is an illustrative example, with round figures chosen to show the mechanism, not a claim about any one brand.

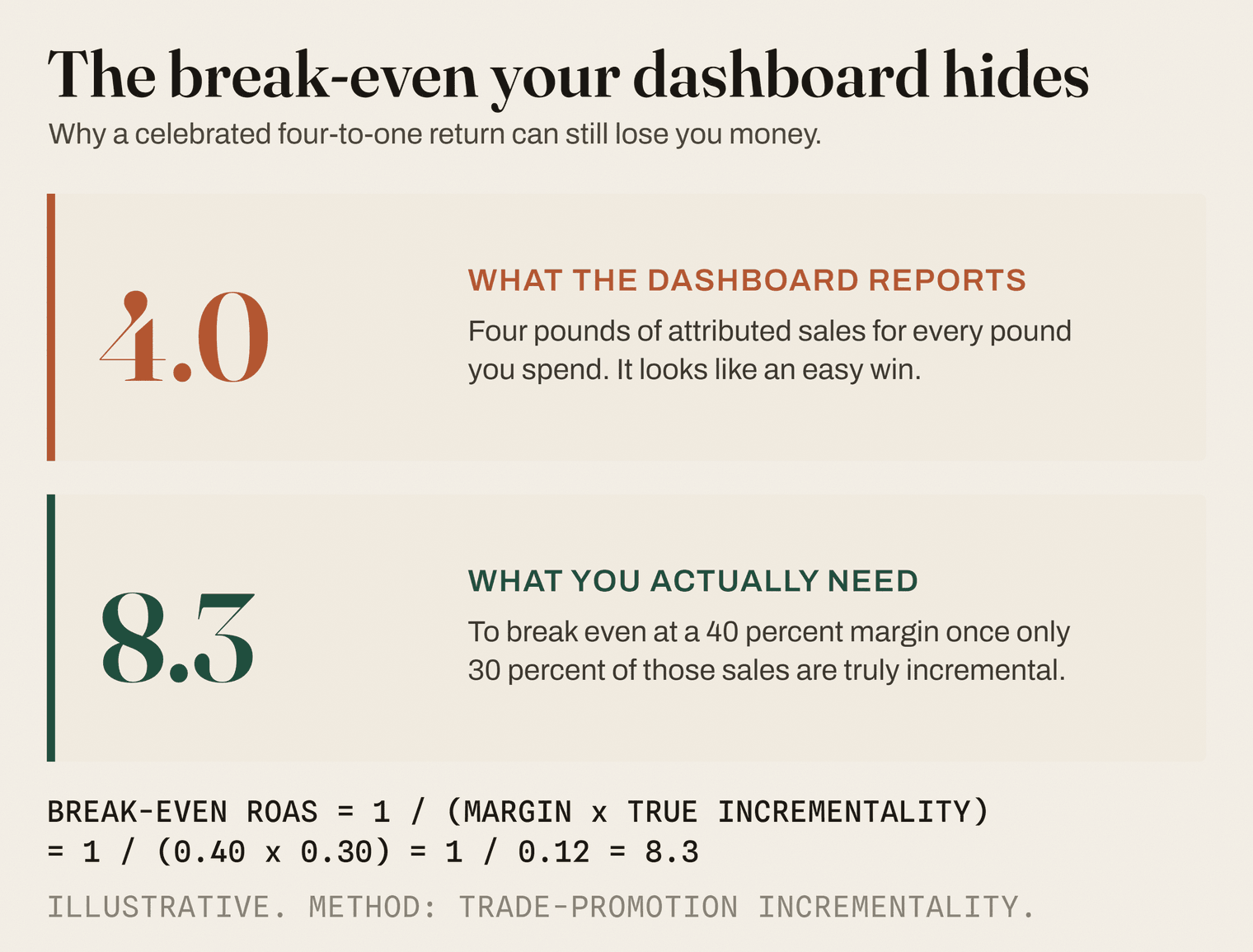

Say you spend 1,000,000 on a retailer's media over a year. The dashboard reports a ROAS of 4.0, so 4,000,000 of attributed sales. Your gross margin is 40 percent. So far, so good.

Now apply the incrementality lesson. Suppose 30 percent of those attributed sales are genuinely incremental, in line with what decades of promotion analysis would predict, and the other 70 percent would have happened anyway. Your true incremental sales are 1,200,000. At a 40 percent margin, that is 480,000 of incremental gross profit. You spent 1,000,000 to earn 480,000. The celebrated "4.0 ROAS" campaign lost you 520,000 once you count only the sales it actually created.

Meanwhile your retailer booked your 1,000,000 of advertising spend at, say, an 80 percent margin, which is 800,000 of near-pure operating profit. Look at where your million went. It became 800,000 of profit for your customer and 480,000 of incremental gross profit for you, and the difference is the cost of buying sales you already owned.

There is a simple rule buried in that arithmetic, and it is worth carrying into your next planning meeting. The ROAS you actually need to break even is one divided by the product of your gross margin and your true incrementality. At a 40 percent margin and 30 percent incrementality, that is one divided by 0.40 times 0.30, so one divided by 0.12, which is about 8.3. You need a reported ROAS of 8.3 just to get your money back, not the 4.0 the dashboard is celebrating. If that sounds harsh, it is the same break-even logic you already run on a promotion. Retail media does not get a different law of physics because it has a nicer interface.

This is the value transfer at the heart of the whole subject. A near-pure-margin pound of profit is migrating from your profit and loss to your retailer's, one plan at a time, and the reported ROAS is the anaesthetic that keeps it from hurting. One supplier-side analysis called retail media, with rare candour, "a polite way to transfer margin from the supplier's P&L into the retailer ecosystem" [10]. Another described the market as an "80 billion dollar tollbooth," warning that "if all you're doing is shifting trade dollars into digital ads, you're just funding retailer margin, not brand growth" [11]. The tollbooth is on a road you built.

Who in your building actually owns this money?

Here is the organisational failure that makes all of the above possible. Ask inside most consumer goods companies who owns retail media, and you will get a shrug dressed as a process.

The trade team does not want it, because it does not deliver the promotional volume they report against. The brand team does not want it, because it does not deliver the reach and equity numbers they are measured on. And neither rushes to fix it for a quiet reason: the cost of wasted retail media never lands on the metric either team is judged by, so for both of them the cheapest move is to leave it in the other's envelope. So it ends up negotiated inside the joint business plan conversation (JBP), where about 38 percent of brands say plan adherence is one of the top three reasons they spend on retail media at all [8]. A large share of this spend is committed not because a business case cleared a hurdle, but because it was in the plan and saying no felt risky. The budget is signed by everyone and owned by no one, which is the exact condition under which money escapes scrutiny. A few of the better-run companies have started to answer this by elevating retail media into an enterprise commerce-media function with real ownership [12], but they are still the minority.

It is also fragmenting. The average brand now runs around six retail media networks and expects to run about eleven by the end of 2026, while operations teams already lose somewhere between 20 and 40 percent of their week to manually stitching together reports that do not add up, because no two networks measure the same way [13]. Adding the eleventh network is rarely a strategy. It is usually compliance, another plan with another media line, and each one is a fresh place for unmeasured spend to hide. The retailers are not all winning either; by their own account, only half of retail media networks hit their goals in a recent year, and most struggle to explain what makes them different [8]. This is not a confident, settled market; it is a land grab with a measurement problem on both sides.

Given versus earned, and the test every trade pound should pass In trade terms we long ago stopped handing money over for nothing. Every pound of trade investment is supposed to pass three tests. Is it efficient, meaning the cheapest way to get the result? Is it effective, meaning the retailer's behaviour would actually change if you withdrew it? Is it defensible, meaning it survives an audit and the competition rules? The best-run companies then push most of that money from given to earned, so the payout scales with performance instead of arriving as a fixed lump sum, with 60 to 80 percent of trade investment made conditional. A conditional deal pays out only when the retailer delivers the agreed uplift, confirmed by the scanner data, not before. Almost no retail media is structured this way today. You pay up front, and the outcome is the retailer's to report. Moving retail media from given to earned is the single most useful thing you can do to it.

The fix is not a new department for its own sake. It is to treat retail media as what it is, a line of trade investment, and to give it the governance trade investment already has. One owner who holds the whole envelope, sitting in the planning conversation rather than scattered across brand and e-commerce. One internal definition of incremental that you, not the network, control. One measurement spine that lets you compare across networks and run holdout tests by default. And one gate the spend has to clear before it goes into a plan: what is the incrementality assumption, what is the break-even, and would this clear the same hurdle we set for a promotion? If it cannot answer, it does not go in the plan. That is not bureaucracy. It is the discipline you already apply to every other pound that crosses to your customer.

So what do you do before the next plan?

You do five things, and none of them require waiting for the industry to fix its measurement. They run in this order on purpose: you cannot measure what you have not named, and you cannot negotiate what you have not measured.

First, name the money. Pull every pound of retail media out of wherever it is hiding, on-site, off-site, the loyalty deals, the in-store screens, and put it in one envelope next to your trade investment, where finance can see it. You cannot govern what you cannot total.

Second, set your own incrementality bar. Decide, as a company, what incremental means and what break-even ROAS you require given your margins, and write it down before the negotiation, not after. Use the rule above. If your margin is 40 percent and you assume 30 percent incrementality until proven otherwise, your hurdle is a reported ROAS around 8.3, and most "wins" will not clear it.

Third, demand a holdout test on your largest commitments. If a network will support a clean test, you finally have real numbers and a reason to spend more where it works. If it will not, you have learned something important about how confident they are in their own product.

Fourth, consolidate. Resist the slide to eleven networks. Put your weight behind the few that can prove incrementality and carry your data cleanly, and make the rest earn their place. The operational time you save is real money, and a smaller, measured portfolio negotiates better than a sprawling, blind one.

Fifth, and this is the one most brands miss, use your leverage. Your retailer now depends on your advertising money for a serious slice of its profit. That dependence cuts both ways. A brand that arrives offering to co-design a proper incrementality test is not being generous; it is setting the standard the retailer's numbers will be judged against, and it is negotiating from proof rather than fear. The same logic that lets a retailer tie media to your shelf can let you tie your media to measurement you trust.

The pushback I expect

"But our ROAS is genuinely strong." Maybe. Run one holdout test and find out. If the lift survives, spend more, with my blessing. If it does not, you just found the most expensive line in your plan.

"Off-site and connected television are real brand building, not just harvesting." Some of it is, and that is exactly why you measure and separate it rather than funding the whole thing on one blended number. Brand building has its own, slower payback, and it should be judged on that, not smuggled in under a sponsored-search ROAS.

"If we do not spend, we lose the shelf." That is the tollbooth, and it is real. But naming it changes the conversation. If media access is really a condition of distribution, then it is a trade term, and it belongs in the trade negotiation with everything else you trade, not in a separate marketing budget with no leverage attached. And you negotiate it from a stronger position than you think, because your advertising money is now material to the retailer's own profit, which is the point I want to leave you with.

"This is marketing's job." The budget is sitting in your joint business plan, funded from trade co-op, and landing on your customer's profit and loss. That makes it a revenue growth management problem, the discipline that already owns trade investment, pricing, and mix. Marketing builds the creative. You own the investment.

What would have to be true for me to be wrong

If retail media were mostly incremental, if its measurement were standardised and comparable across networks, and if the money were genuinely net-new media budget rather than redirected trade, then this would be a media buy and not a margin transfer, and my whole argument would soften into "spend carefully." Watch for it. The certification work that began in late 2025, with the first networks earning independent accreditation [14] and a new in-store measurement standard [15], is the start of exactly that credibility floor. The day a network hands you an audited, comparable, incrementality-based number is the day retail media grows up. We are not there yet. Until we are, govern it like the trade money it is.

Signals

- Walmart's global advertising business reached about 6.4 billion dollars in 2025, up 46 percent, and advertising and membership together made up roughly a third of its operating profit in the quarter. https://www.adexchanger.com/commerce/walmarts-ad-revenue-totaled-6-4-billion-in-2025-as-the-ecom-flywheel-started-to-spin/

- Amazon's advertising passed about 68 billion dollars in 2025; one analysis argues that without that high-margin income, its retail business "would be increasingly unprofitable." https://www.marketplacepulse.com/articles/amazons-expansive-advertising-breaks-new-records

- The Interactive Advertising Bureau published an in-store retail media measurement framework in December 2025, defining a verified impression as Play plus Presence plus Pairing, the first real standard for the store floor. https://www.iab.com/guidelines/framework-for-maturing-in-store-media-measurement/

- Albert Heijn became the first network certified under the IAB Europe retail media programme in September 2025, and Walmart Connect earned Media Rating Council accreditation for sponsored search in October, opening a certification era. https://www.exchangewire.com/blog/2025/09/24/iab-europe-certifies-albert-heijn-as-first-retailer-under-the-retail-media-certification-programme-audited-by-abc/

- Sainsbury's announced its Nectar360 Pollen retail media platform in June 2025, with launch planned for later that year, a sign of how fast the European networks are still being built out. https://www.retailgazette.co.uk/blog/2025/06/sainsburys-retail-media/

References

- Walmart, fourth-quarter and full-year fiscal 2026 earnings release (global advertising grew 46 percent to nearly 6.4 billion dollars), with the one-third-of-operating-profit disclosure reported by AdExchanger, February 2026. https://stock.walmart.com/_assets/_461d6b46a29d437b51015f942ff9bb4e/walmart/db/938/9972/earnings_release/Earnings+Release+(FY26+Q4).pdf and https://www.adexchanger.com/commerce/walmarts-ad-revenue-totaled-6-4-billion-in-2025-as-the-ecom-flywheel-started-to-spin/

- VideoWeek, citing GroupM This Year Next Year, December 2024, on retail media overtaking global television (about 176.9 billion dollars, 15.9 percent of global ad spend). https://videoweek.com/2024/12/09/digital-economy-consolidates-around-a-few-massive-platforms-in-groupm-forecast/

- Dentsu global advertising forecast, December 2025 (retail media the fastest-growing channel at about 14 percent). https://www.dentsu.com/news-releases/global-ad-spend-set-to-surpass-one-trillion-for-the-first-time-in-2026-as-the-algorithmic-era-redefines-growth

- eMarketer US retail media forecast, H2 2025 update, via Fugo (about 58.8 billion dollars in 2025 toward 69.3 billion in 2026; Amazon roughly three quarters of US retail media; off-site growing about twice as fast as on-site). https://www.emarketer.com/content/retail-media-ad-spending-forecast-trends-h2-2025 and https://www.fugo.ai/blog/retail-media-growth-statistics-trends/

- Marketing Dive, Amazon annual advertising revenue (about 68 billion dollars in 2025), February 2026. https://www.marketingdive.com/news/amazon-annual-ad-revenue-passes-68b-boosted-by-full-funnel-strategy/811569/

- Marketplace Pulse, Amazon advertising records, August 2025. https://www.marketplacepulse.com/articles/amazons-expansive-advertising-breaks-new-records

- Kroger, Form 8-K, alternative profit businesses (about 1.35 billion dollars operating profit, media up 17 percent), February 2025. https://www.sec.gov/Archives/edgar/data/0000056873/000110465925021187/tm258221d1_ex99-1.htm

- Skai and Path to Purchase Institute, State of Retail Media (joint-business-plan funding at about 47 percent, plan adherence a top-three driver for about 38 percent, incrementality the top barrier, about 56 percent rating their own measurement strong, and the retailer-side survey where only half met their goals). https://skai.io/blog/the-2026-state-of-retail-media-dsp-ctv-and-social-commerce-accelerating-beyond-the-shelf/

- The Drum, on retail media measurement and return on ad spend, November 2025. https://www.thedrum.com/opinion/the-how-brands-grow-dogma-wants-to-have-a-word-with-retail-media

- Woodridge Retail Group, on retail media return on investment for suppliers, March 2026. https://www.woodridgeretailgroup.com/post/retail-media-roi-for-cpg-suppliers

- Public Label Agency, on retail media as a tax on brands, February 2025. https://blog.publiclabelagency.com/public-label/retail-media-the-new-tax-on-cpg-brands

- Wiss, on consumer goods companies elevating retail media to enterprise functions, February 2026. https://wiss.com/cpg-giants-pivot-to-retail-media/

- Improvado, on retail media network count and reporting overhead. https://improvado.io/blog/top-retail-media-networks

- ExchangeWire, Albert Heijn certified as the first network under the IAB Europe retail media programme (September 2025), with Walmart Connect earning Media Rating Council accreditation for sponsored search in October 2025. https://www.exchangewire.com/blog/2025/09/24/iab-europe-certifies-albert-heijn-as-first-retailer-under-the-retail-media-certification-programme-audited-by-abc/

- Interactive Advertising Bureau, framework for maturing in-store retail media measurement (the Play, Presence, Pairing standard), December 2025. https://www.iab.com/guidelines/framework-for-maturing-in-store-media-measurement/