Private Label Is Not a Price War

The store brand is not a cheap copy, it is a better business model. Do not answer a power shift with a discount.

The short version

- Private label just crossed half of all grocery units in Europe's six biggest markets and set a United States record at 282.8 billion dollars. It still holds only 42 percent of European value, and the gap between units and value is the pricing power you have left.

- This is not really a product fight. The retailer has built a better business model. It owns the richest consumer data and, through retail media at margins near 70 percent, the most profitable demand engine in the store. Private label is how it turns both into control of the category and leverage over you.

- The own brand got good, and it is now being picked up at the top of the income scale, not just the bottom. The cheap-copy defence has expired.

- Matching the store brand on price is usually a trap, and it is worse the stronger your brand. Closing the gap through smaller packs or genuine cost reduction is a different and legitimate move.

- Your best argument in the buyer's office is not a lower price. It is that your brand still puts more cash in the retailer's till per foot of shelf than the own brand does.

- The trend is structural and began long before the cost-of-living squeeze, but the recent jump is partly reversible. The share you keep depends on whether you reinvest in the brand now, not on whether incomes recover.

- So the job is triage by category. Fight where the moat is still yours, cede the bottom tier on purpose where it is not, and compete on ground the retailer cannot reach.

How did the store's own brand end up owning half the shelf?

Here is a question for your next leadership meeting. Name the three biggest consumer goods companies in the United States by own-brand sales. They are a grocer, a warehouse club, and a mass retailer. Kroger's own brands turned over more than 32 billion dollars in 2024, which on its own would rank around the ninth-largest packaged goods company in the country [1]. Costco's Kirkland Signature is about 28 percent of everything Costco sells [2]. None of these giants runs a Super Bowl ad, and they do not need to. They already own the shelf the ad would send you to.

That is the shift hiding behind the headline number, and the headline number is large enough on its own. In April 2026 Circana reported that private label had crossed 50 percent of grocery units across Europe's six biggest markets for the first time, worth 324 billion euros [3]. In the United States, store brands hit a record 282.8 billion dollars in 2025, grew nearly three times faster than national brands, and took 47 percent of all the dollar growth in the year [4]. Half of Europe's trolley, by volume, is now the store's own.

The instinct is to read this as a recession story, a wave of trading down that will recede when wages catch up. The best evidence says otherwise. The most careful academic work on the question, a study of 132,000 American households across the last big downturn, found that the swings driven by income are far smaller than the industry assumes, and that underneath them sits a steady structural climb of roughly half a share point every year that runs straight through good times and bad [5]. The cost-of-living shock did not start this; it accelerated a climb that was already well under way.

So the useful question is not whether private label is big. It is why it keeps growing when, by the old playbook, it should not.

Unit share versus value share. Two numbers describe the same shelf. Unit share is how many packs sold are own-brand. Value share is how many of the pounds and euros are. In Europe private label is 50 percent of units but 42 percent of value, an eight-point gap [3]. That gap exists because shoppers still pay more for the national brand. It is, quite literally, the premium your brand still commands. Watch the value line, not the unit line. The day the value gap closes is the day the pricing power is gone.

When did private label stop being the cheap copy?

For thirty years the defence wrote itself. The store brand was the yellow-pack imitation, cheaper because it was worse, and the shopper who could afford better bought better. That world is gone. In McKinsey's recent food and beverage work, more than three-quarters of shoppers now rate private label as equal to or better than the national brand on quality [6]. Premium own-brand lines, the ones that cost more than the mainstream national brand, are now about 40 percent of all private-label spending in the United States [7]. Tesco Finest and Sainsbury's Taste the Difference each sell more than two billion pounds a year, competing on how good they are, not how cheap.

The part that should worry you most is who is buying. The easy assumption is that private label is a floor for people under financial pressure. The data has flipped that. In Simon-Kucher's 2026 global study, 44 percent of higher-income American shoppers, those earning five thousand dollars a month and up, said they were buying more private label than the year before, against 34 percent of lower-income shoppers [8]. The growth is being led from the top, by people who could buy your brand and are choosing not to. Around the world, half of shoppers now say they buy more own-brand than they used to [9].

This is the quiet death of the trade-up. The brand business has always rested on a simple promise: as people get a little richer, or want to treat themselves, they climb from the store brand to yours. When the better-off shopper is climbing the other way, and feels good about it, the escalator you were counting on is running in reverse.

The old defence assumed the shopper would eventually want better, and that better meant you. Neither half holds the way it used to.

Your fastest competitor now owns the shelf and the data

There is a deeper reason the store brand stopped being a copy. It stopped copying. For most of retail history the brand led and the own-brand followed, a season or two behind, cloning last year's winner. That lag has collapsed, and in places it has inverted. In McKinsey and EuroCommerce's 2026 read of European grocery, private label now accounts for around 70 percent of new food product launches, and retailers that gave their own brands more shelf space gained category share two to three times more often over six years than those that did not [10]. The own-brand is not trailing the innovation. In a lot of aisles it is the innovation.

What changed is the data. Your brand sees the market through a rear-view mirror: syndicated panels, bought a few weeks late, showing what already happened across a sample. The retailer sees the windscreen, every basket, every loyalty card, in real time, for tens of millions of shoppers. AlixPartners put it bluntly: retailers hold the most valuable asset for building a brand, millions of records of who actually buys what, next to what, and how often, something the manufacturer can only dream of [11]. Mercadona runs co-innovation centres that test thousands of products a year with real shoppers. Walmart used its own purchase data to design bettergoods so precisely that its ice cream buyers skew heavily towards the younger shoppers Walmart wanted to win.

Layer artificial intelligence on top and the gap widens. New synthetic testing tools can return a read on whether shoppers will buy a concept in under a day, against the six to eight weeks of traditional research [11]. The retailer with the data and the speed gets to shelf while you are still briefing the agency.

Be precise about where this bites, though, because it does not bite everywhere. The retailer's edge is sharpest in categories where products are close substitutes and the win is reliable quality at a lower price. It is weakest where the product is genuinely hard, where the breakthrough takes years of research, or where the brand carries meaning the data cannot manufacture. We will come back to that high ground, because it is where the fight is winnable. Before we get there, we need to look at the fight you cannot win.

Why does cutting your price to match usually make it worse?

When share slips to the own-brand, the reflex is older than any of us: close the gap. Drop the price, fund another promotion, narrow the distance to the store brand until the shopper comes back. It feels like action, and it is usually the most expensive mistake on the table. The arithmetic shows why, and there is one real exception I will come to.

The price gap and the price-quality cue. The gap is the distance between your shelf price and the own-brand's. It does two jobs at once. It is the toll a shopper pays to choose you, and it is a signal. A wide, steady gap tells the shopper your product is worth more. Cut it sharply and you do not just earn less per pack, you whisper that the two products were always the same. Worse, the new low price becomes the shopper's reference point, the number they now think your product is "really" worth. Shoppers notice a change of more than about 10 to 15 percent, so a deep cut is easy to make and hard to take back.

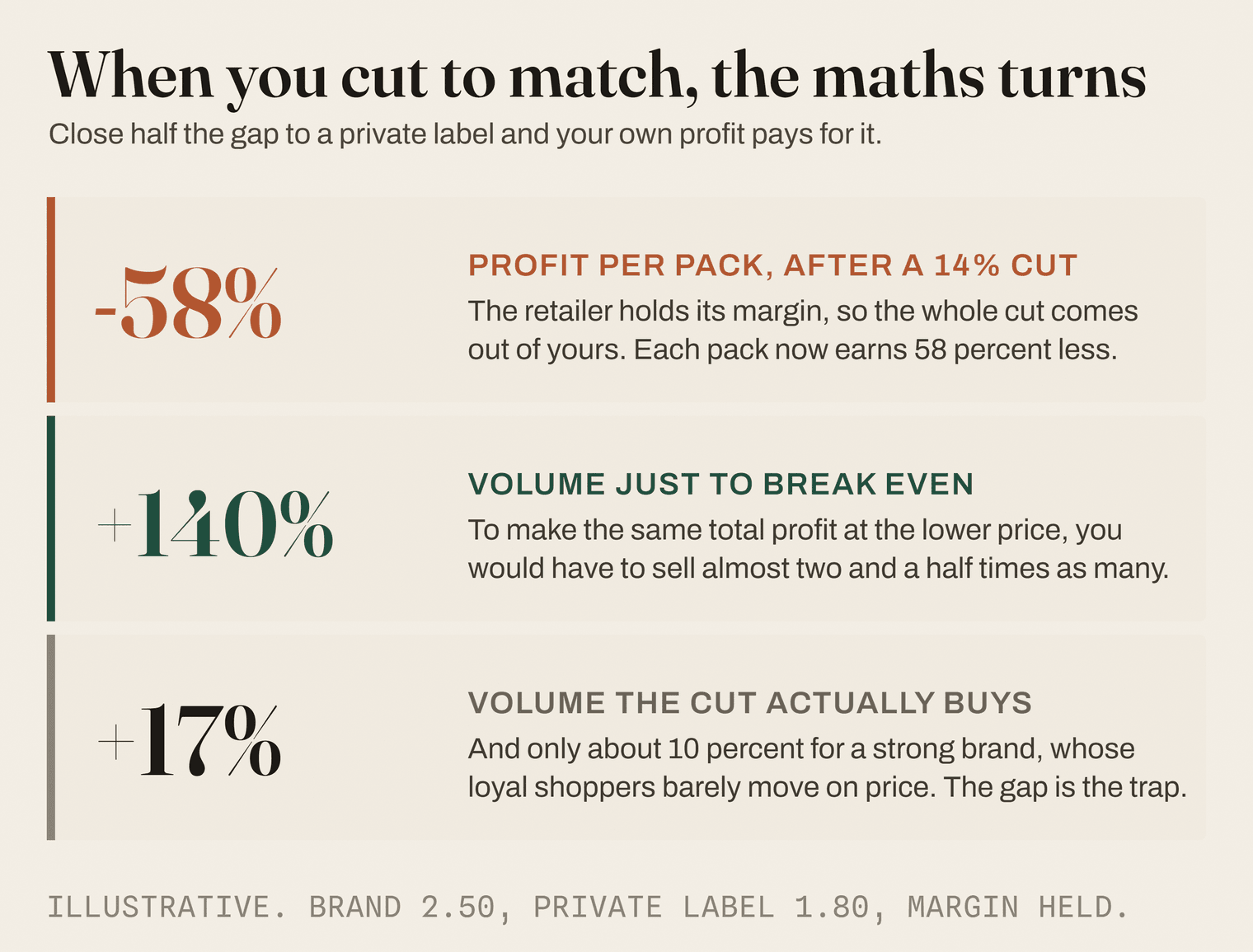

Walk the numbers. (These are illustrative, but they reconcile.) Your brand sells at 2.50, you net 1.50 from the retailer, your cost is 0.90, so you make 60 pence a pack. At a hundred packs that is 60 pounds of profit. The own brand sits at 1.80, so you are 38.9 percent dearer. You decide to close half that gap, dropping your shelf price to 2.15, a cut of 14 percent. The retailer holds its cash margin, so the whole cut comes out of your net, which falls to 1.15. Your profit per pack is now 25 pence, down 58 percent. To stand still on total profit you would need to sell 240 packs, a 140 percent jump in volume.

Will the cut deliver that? Not remotely. Take an ordinary brand whose volume moves about 1.2 percent for every 1 percent of price. A 14 percent cut buys you roughly 17 percent more volume, about 117 packs, worth 29 pounds against the 60 you started with. You have lost half your profit to sell a few more units, and you have reset the shopper's idea of what you cost.

Now the part that catches people out. The stronger your brand, the worse this gets. A strong brand has loyal shoppers whose volume barely moves on price, say 0.7 percent for each 1 percent. That same 14 percent cut now buys only about 10 percent more volume, around 110 packs, worth 27 pounds. You gave away more and got back less, because the thing that makes a strong brand valuable, that its shoppers do not flinch at the price, is exactly the thing that makes discounting it a donation. The premium does not protect you in a price war; it is the very thing you end up setting on fire.

There is one real exception, and it matters. Closing the gap through structure rather than through everyday price is a different move. Bringing in a smaller entry pack, or a genuine cost reduction that lets you hold margin at a lower price, gives the budget shopper a way to stay with you without resetting the reference price of your main line. Mondelez has been doing exactly this, adding pack sizes at three and four dollars to win back units without slashing the hero [12]. The trap is not "never narrow the gap." The trap is narrowing it with a discount, in a category where the shopper already thinks the two products are the same.

Why are you paying rent to the rival on your own shelf?

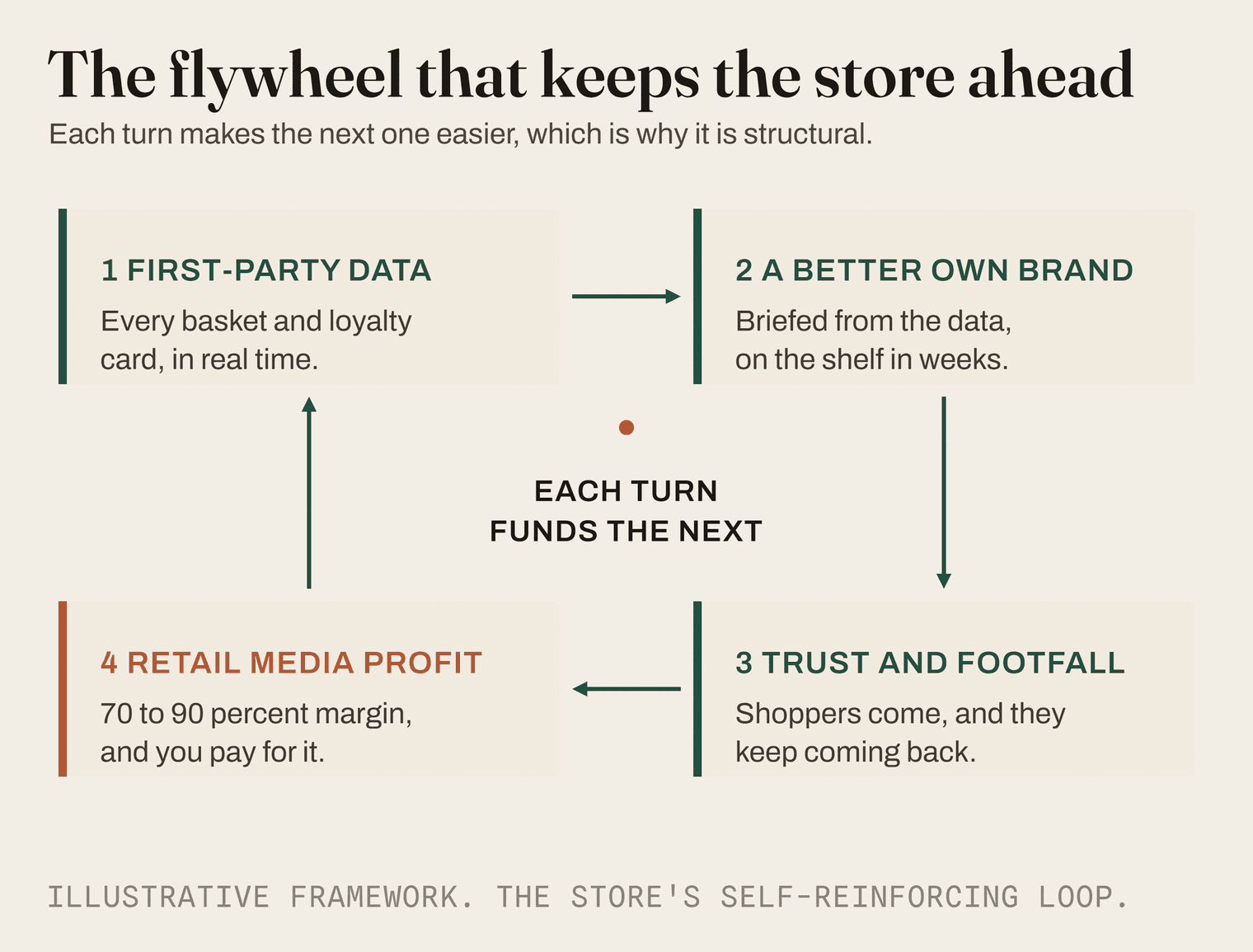

Here is where the picture stops being a shelf and starts being a system. The retailer is not just selling against you with its own brand. It is running a machine, and private label is one gear in it.

The machine works like this. First-party data builds a better own-brand. The better own-brand wins trust, share, and footfall. That traffic and that loyalty deepen the data and pull in more shoppers, which makes the retailer's advertising inventory more valuable. And that advertising, retail media, is the most profitable thing in the building. On-site retail media runs at margins of roughly 70 to 90 percent, against the 3 to 4 percent a grocer makes selling groceries [13]. Walmart's advertising business is under one percent of its revenue and yet more than a fifth of its operating profit [14]. The profit from selling you visibility then funds sharper prices on the own-brand, and the gear turns again.

So you are now paying your competitor twice. Once when the own-brand takes your volume, and again when you buy retail media to be seen, often in a sponsored slot right next to that own-brand. No manufacturer has yet published the full bill, the retail-media cheque and the private-label volume loss added up in the same category, but any commercial leader can feel it in the profit and loss account.

This reframes where the profit is going, and it is not where the margin headlines suggest. Yes, big manufacturers still report operating margins of 15 to 20 percent against a grocer's 2 to 4 percent [15][16]. But the manufacturer's margin is under steady pressure while the retailer has bolted on a high-margin profit engine that the reported grocery margin does not even capture. The pool of profit in the category is migrating, from you to the retailer, and inside the retailer from the shelf to the screen.

The profit pool and the cash-profit paradox. The profit pool is the total profit a category throws off, and the real contest is who keeps which slice of it, the brand or the retailer. Retailers do not push private label simply because the percentage margin is higher. The percentage margin can be higher on the own-brand while the cash profit is higher on your brand, because your brand sells at a higher price. A retailer can make 40 percent on your pack and 43 percent on the own-brand, and still take more actual money from yours. Delisting you would lift the margin percentage and shrink the category's cash profit. That is your lever, and most brands never pull it.

Walk that one too. (Illustrative again, and it reconciles.) One facing, one week. Your brand: it sells at 2.00, the retailer buys it at 1.20, so it makes 80 pence a pack, a 40 percent margin; it shifts 90 packs, so 72 pounds of cash, and you pay 8 pounds for the sponsored slot, so the retailer earns 80 pounds from your space. The own-brand: it sells at 1.40, the retailer buys it at 0.79, so it makes 61 pence a pack, a 43.6 percent margin; it shifts 100 packs, so 61 pounds, and it pays itself nothing for media. Your facing earns the retailer 80 pounds. The own-brand earns it 61. You are 31 percent more valuable to that shelf, despite the lower headline margin. Swap you out for another own-brand facing and the retailer's category cash profit falls, even as the margin percentage on the planogram ticks up.

That number, cash profit per facing, is the most underused sentence in the joint business plan. There is one more layer beneath it, and it is the real reason the gap is so hard to hold. The mere existence of a credible own-brand changes the negotiation. A study of one United States category modelled what happens when the retailer has a good private label sitting in the wings: it earned about 18 percent more profit on the national brand's own sales, because the own-brand is the walk-away option that makes every demand on you stick [17]. Private label is not only a product on the shelf, it is the retailer's best card in the room, played every time you sit down.

So do you fight, or do you cede?

If you cannot win on price and you are funding your rival's growth, the only sensible conclusion is that you should not be defending everything. The best commercial leaders are getting comfortable with a word the brand world hates: cede. Nestle has been pruning hard, moving to sell its remaining ice cream business to Froneri in early 2026 and concentrate its force on coffee, pet, nutrition, and confectionery [18]. Meanwhile the retailers are telling you where they are coming next, if you listen: Ahold Delhaize has said it wants own-brand to reach 45 percent of sales by 2028, and Albertsons is aiming for 30 percent over time, up from around 26 percent now [19]. When your customer announces a target like that, treat it as a map of where to disinvest.

Ceding is not surrender, it is triage, and the test is whether the moat is real.

Fight or cede, by category. Four questions decide it. Can the product be genuinely differentiated, or is it close to a commodity? Is this category core to who you are, or an outpost? Do you have the data and the innovation speed to keep moving faster than the own-brand? And how hard has the retailer said it will push its own label here? Two or more answers pointing to "weak" is a signal to cede the bottom tier deliberately, harvest it, and move the money. Two or more pointing to "strong" is a signal to fight, but to fight on the ground the retailer cannot take.

Run a category through it. Take a household staple where your brand is a mid-tier player, the product is close to a commodity, it is not core to who you are, your data and innovation edge is thin, and your retailer has just announced an own-brand push. That is four answers pointing the same way, so the move is not to defend it with deeper promotions. It is to harvest it: stop the promotional spend, hold the list price, accept a slow decline in share, and move the freed marketing money to the tier where a real difference is still possible. Ceding on purpose is how you fund the fight you can win.

That ground is real, and the evidence marks it out. The retailer's data and speed win the fast, substitutable kind of innovation, the new flavour and the better-value reformulation, but they do not buy the multi-year research or the brand meaning the high ground is built on. Private label stays weak where the product carries meaning rather than just function. It is close to absent in spirits and barely present in fine fragrance, because those purchases are about identity and occasion, not price per litre. Simon-Kucher finds brands strongest exactly where emotion, experience, and identity drive the choice, in drinks, in personal care, in pet [20]. Even Amazon, with the deepest data and pockets on earth, quietly cut its own private-label range from dozens of brands to under twenty and watched its share of United States retail drift down to under one percent, because the model works for batteries and basics and fails in anything design-led or emotional [21]. And no own-brand can do the one thing your brand does by definition: travel. Kirkland Signature cannot be bought outside Costco. Your brand is on every shelf, in every market, building equity that compounds across all of them. The store brand is captive to one retailer; your brand is not.

Which leads to the move most brands miss. The strongest answer to a competitor who owns the shelf is sometimes to stop fighting on the shelf. Build the thing the retailer cannot replicate: a reason to be chosen that lives in the product's real innovation, in a brand people feel something about, in a relationship you own directly. You will not out-data the retailer inside its own store, so be the brand its data cannot invent.

One last decision sits underneath all of this, and almost nobody discusses it openly. A large share of private label is made by manufacturers, and some of it is made by brand owners themselves, quietly, in the same factories [22]. The temptation is obvious: the volume is incremental, the line is already running. The strategic cost is just as real, because you are funding and improving the very competitor eating your brand, and you are handing the retailer a more credible walk-away option in your own negotiation. Most of the big brands have drawn the line at non-core categories for a reason. It is a board-level question, not a plant-utilisation one, and it deserves to be asked out loud.

Is this structural, or just the cost-of-living hangover?

I have argued that this is structural, and I want to be exact about what I mean, because the lazy version of that claim is wrong. The long-run climb is structural. It predates the inflation shock, it is built on quality, data, and the retailer's economics, and none of those reverse when wages recover. But the extra jump of the last two years is partly a cost-of-living effect, and part of it is reversible. Private label has given share back before. In the United States it peaked near 17 percent in the early 1980s downturn and fell back to under 15 percent by the mid 1990s as brands reinvested [23]. In the pandemic, when shoppers fled to the familiar, national brands actually grew a touch faster than private label for a stretch [24]. The level is not a one-way ratchet.

The thing that decides how much you keep is not the economy. It is you. The research on past downturns is unusually clear and unusually encouraging: the manufacturers that held or regained share were the ones that kept investing in their brands and their innovation through the slump, rather than cutting marketing to protect the quarter and discounting to chase volume. The recovery of share is earned in the downturn, by the brands that behaved as if the moat was worth defending.

The pushback I expect

Let me take the three I hear most, head on. "Our retailer will delist us if we do not fund retail media." Maybe, but your leverage is the cash-profit-per-facing number above; make the buyer confront what delisting does to category cash profit, and price the media against the sales it actually causes, not against the fear. "We tried differentiation and we still lost share." Then you were probably defending a commodity tier where differentiation cannot live; the answer there is to cede that tier on purpose and concentrate the innovation where a difference is possible. "Private label always falls back when the economy turns." At the trend level, no, it does not fall back. The recent spike can recede, but only if you do the work now, which is the whole point.

What would change my mind

I would accept I am wrong on either of two specific tests. If European private-label value share, the value line and not the unit line, falls by half a percentage point or more over any rolling two-year stretch before the end of 2027, the structural case is weaker than I think. Or if, by the end of 2027, at least two of the twenty largest global manufacturers report a real, sustained recovery of volume share against own-label, in a category where private label is above 35 percent, and they credit brand investment rather than a rising market, then the "you cannot win it back" half of the argument fails. Either result is observable, and I will revisit this in public if it happens.

For now, the runway points the other way. In the Middle East and North Africa, private label is still in low single digits while shopper acceptance already runs above 80 percent. The shelf that took thirty years to tip in Europe can tip a great deal faster where the retailers have learned how. The own-brand has not finished. The question on your desk is not whether it is coming. It is which parts of your portfolio are worth defending when it does, and whether you will spend the next two years building moats or cutting prices.

Signals

- Private label crossed 50 percent of grocery units across Europe's six largest markets for the first time, worth 324 billion euros (Circana, April 2026): https://www.circana.com/post/private-label-reaches-record-50-unit-share-across-europe-s-six-biggest-grocery-markets

- United States store-brand sales hit a record 282.8 billion dollars in 2025, growing nearly three times faster than national brands (PLMA and Circana, January 2026): https://www.plma.com/article/us-private-label-industry-reached-2828-billion-sales-2025

- Walmart's bettergoods reached roughly 500 million dollars in its first year, the retailer's biggest private-brand food launch in two decades (Grocery Dive, June 2025): https://www.grocerydive.com/news/walmart-cfo-talks-private-brand-delivery-growth/751146/

- Higher-income American shoppers are now adopting private label faster than lower-income ones, 44 percent against 34 percent buying more year on year (Simon-Kucher, 2026): https://www.simon-kucher.com/en/insights/private-labels-upmarket-moment-affluent-us-shoppers-shift-private-label-and-arent-trading

- Amazon cut its private-label brands from dozens to under twenty as its share of United States retail slipped below one percent, a reminder the model fails in differentiated categories (PMG, 2024): https://www.pmg.com/insights-and-news/amazons-private-label-market-share-shrinks-by-6-year-over-year-in-q1-2024

References

- Kroger, 2025 Responsible Business Report. https://www.thekrogerco.com/wp-content/uploads/2025/10/Kroger-Co-2025-Responsible-Business-Report.pdf

- PLMA, Costco private-brand sales reach 28 percent. https://plma.com/article/costco-private-brand-sales-reach-28

- Circana, private label reaches record 50 percent unit share across Europe's six biggest grocery markets, April 2026. https://www.circana.com/post/private-label-reaches-record-50-unit-share-across-europe-s-six-biggest-grocery-markets

- PLMA and Circana, US private label reached 282.8 billion dollars in 2025, January 2026. https://www.plma.com/article/us-private-label-industry-reached-2828-billion-sales-2025 (share-of-growth figure from the 2026 full report: https://www.plma.com/sites/default/files/files/2026-01/plma-2026-report.pdf)

- Dube, Hitsch and Rossi, Income and the private-label share, NBER Working Paper 21446. https://www.nber.org/system/files/working_papers/w21446/w21446.pdf

- McKinsey, The State of Food and Beverage 2026. https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/state-of-food-and-beverage

- Numerator, the price gap between private label and national brands, May 2025 (survey fielded March 2025). https://www.numerator.com/press/price-gap-growing-between-private-label-and-national-brands-99-of-u-s-households-now-purchasing-private-label-products-numerator-reports/

- Simon-Kucher, private label's upmarket moment, Global Shopper Study 2026. https://www.simon-kucher.com/en/insights/private-labels-upmarket-moment-affluent-us-shoppers-shift-private-label-and-arent-trading

- NielsenIQ via FoodNavigator, private label surges on price and quality, June 2025. https://www.foodnavigator.com/Article/2025/06/25/private-label-surges-winning-on-price-and-quality/

- McKinsey and EuroCommerce, The State of Grocery Retail Europe 2026. https://www.mckinsey.com/industries/retail/our-insights/state-of-grocery-europe-report

- AlixPartners, five key pitfalls to avoid when expanding private brands, 2025. https://www.alixpartners.com/insights/102jx4h/five-key-pitfalls-to-avoid-when-expanding-private-brands/

- AlixPartners, revitalizing CPG performance, lessons from market leaders, 2024. https://www.alixpartners.com/insights/102jlox/revitalizing-cpg-performance-lessons-from-market-leaders/

- Mirakl, how retail media networks make money (margin ranges). https://www.mirakl.com/blog/how-do-retail-media-networks-make-money

- Marketplace Pulse, Walmart's advertising revenue, 2026. https://www.marketplacepulse.com/articles/walmarts-advertising-revenue-is-outpacing-amazons

- Procter and Gamble, fourth quarter and fiscal year 2025 results. https://www.pginvestor.com/news/news-details/2025/PG-Announces-Fourth-Quarter-and-Fiscal-Year-2025-Results/default.aspx

- Ahold Delhaize, full year 2024 results (retail operating margin). https://www.aholddelhaize.com/investors/

- Gross, private labels and retailer bargaining power, seminar paper, 2019. https://www.anderson.ucla.edu/sites/default/files/documents/areas/fac/marketing/Seminars/Fall%202019/Private%20Labels.pdf

- Nestle, full year 2025 results and the planned sale of its ice cream business to Froneri, February 2026. https://www.nestle.com/media/pressreleases/allpressreleases/full-year-results-2025

- Albertsons private-label penetration target, Grocery Dive, 2026, and Ahold Delhaize own-brand ambition. https://www.grocerydive.com/news/albertsons-private-label-penetration-grocery-value/802837/

- Simon-Kucher, the rise of private label, why brands must redefine their worth, 2026. https://www.simon-kucher.com/en/insights/rise-private-label-why-brands-must-redefine-their-worth

- PMG, Amazon's private-label market share shrinks, 2024. https://www.pmg.com/insights-and-news/amazons-private-label-market-share-shrinks-by-6-year-over-year-in-q1-2024

- FoodIndustry.com, the US private-label food manufacturing system, January 2026. https://www.foodindustry.com/reports/the-u-s-private-label-food-manufacturing-system/

- Quelch and Harding, brands versus private labels, fighting to win, Harvard Business Review, 1996. https://hbr.org/1996/01/brands-versus-private-labels-fighting-to-win

- L.E.K. Consulting, retail private label (2020 national-brand outperformance). https://www.lek.com/sites/default/files/PDFs/retail-private-label.pdf