How Brands Really Grow: Easy to Buy, Not Easy to Love

Growth comes from more buyers, not deeper loyalty. Most of your marketing money is aimed at the people you already have.

The short version

- Growing brands almost all grow the same way: by adding buyers. About 80 percent of growing brands worldwide widen their buyer base, and across hundreds of categories penetration tracks revenue while how often people buy barely moves.

- Loyalty is mostly your market share wearing a disguise. Bigger brands look more loyal because they have more buyers, not the other way round, so in everyday categories chasing loyalty is chasing an output, not a lever.

- Yet brand owners now put about half their marketing money into loyalty and customer relationship management, and a rising share into precise targeting, all aimed at the buyers they already have. That is the loyalty-tech paradox.

- The reason is measurement, not merit. Loyalty and targeting hand you a number to report; reach and distribution are slower to attribute, so the dashboard wins the budget.

- What loyalty spend actually buys is far less than the business case claims, because your best customers were always going to join the programme. Correct for that and the lift mostly vanishes.

- Being easy to buy beats being easy to love. The default beats the preference, distribution moves sales harder than advertising, and the direct-to-consumer brands most admired for being loved had to get into physical shops to grow.

- Loyalty is not always wrong. In subscription and direct-to-consumer models, in mature categories almost everyone already buys, in identity categories, and as a defensive floor where every rival runs a programme, retention earns its place. The skill is knowing which game you are in.

Why do growing brands almost always grow the same way?

Here is the most reliable finding in all of marketing, and the one most likely to be ignored in your next planning round. There are only two ways any brand can sell more: get more people to buy it at all, which is penetration, or get the people who already buy it to do so more often, which is frequency. Almost all real growth comes from the first. When Kantar tracked which brands grew across thirteen years of global shopper data, about 80 percent of the ones that expanded did it by adding buyers, not by getting their existing buyers to buy more often [1]. In Asia the figure was 88 percent, in China it was effectively all of them [1]. The Ehrenberg-Bass Institute found the same pattern across hundreds of categories: how many people buy you tracks your revenue almost perfectly, while how often they buy barely moves from year to year [2]. Penetration is the engine that drives revenue, and frequency mostly just rides along.

This sounds obvious until you see what it does to the loyalty story. The uncomfortable truth, established so many times it is treated as a law, is that loyalty is mostly a by-product of size. Bigger brands have more buyers and, because they have more buyers, slightly more loyal ones too. The pattern is so regular it has a name, double jeopardy, and it means a small brand is punished twice: fewer buyers, and those buyers a little less devoted [3]. The kicker is the direction of causation. You do not get big by being loved; you look loved because you got big. Chase loyalty in an everyday category and you are chasing the scoreboard, not the game.

A quick word on scope, because this is where the argument is most often misread. I am talking about consumer-goods brand owners, the people who make the things on the shelf. Retailer schemes like a supermarket Clubcard, and platform memberships like a delivery subscription, run on different economics and are a separate conversation. Hold that thought; it matters later.

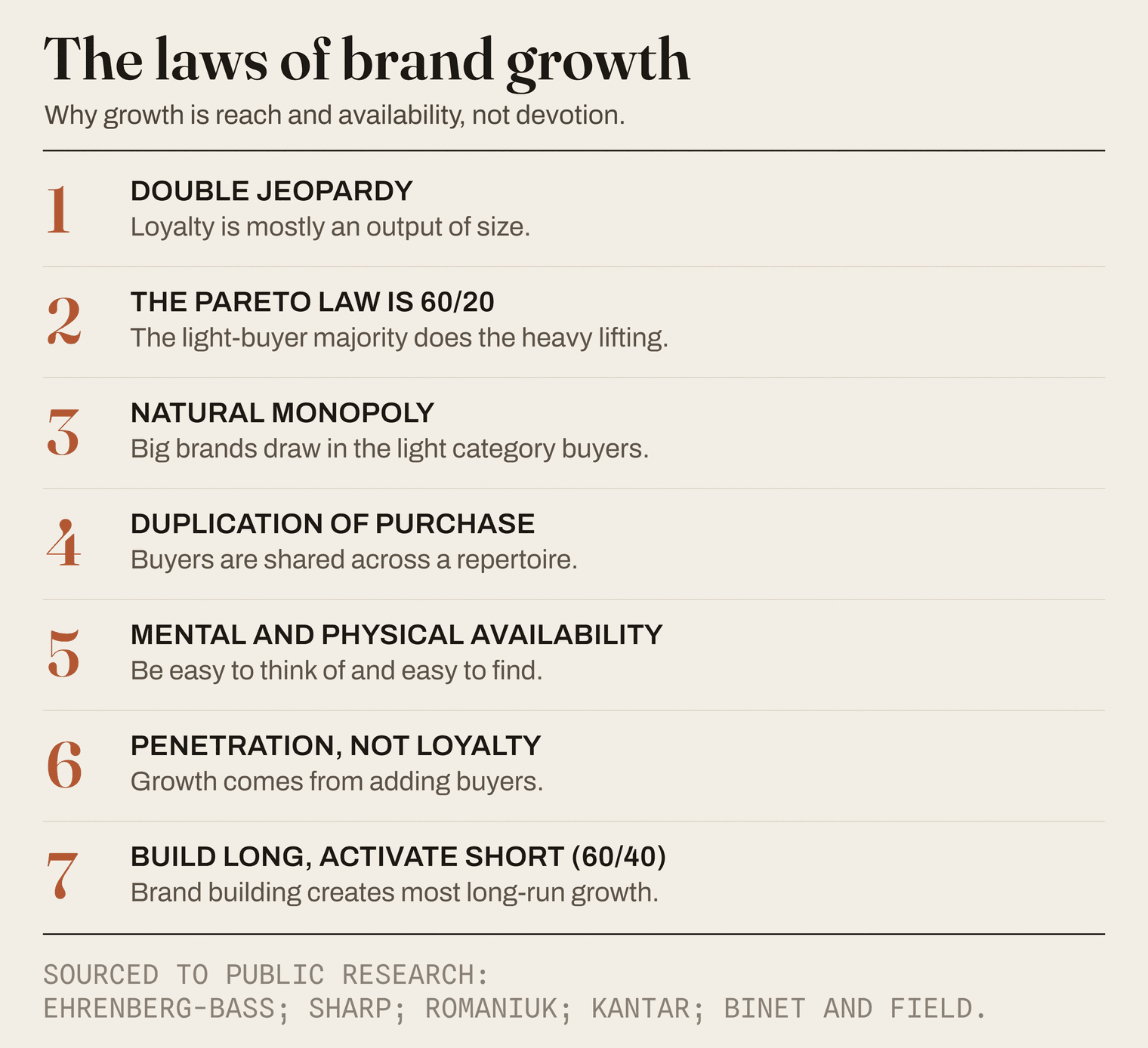

The laws of brand growth. The modern science of how brands grow is well documented, most of it from the Ehrenberg-Bass Institute, with Binet and Field on the budget split. Seven findings carry the weight. One, double jeopardy: loyalty is mostly an output of size, because smaller brands have fewer buyers who are also slightly less loyal. Two, the Pareto law is nearer 60/20 than 80/20, so the light-buying majority matters more than the superfans. Three, the natural monopoly law: bigger brands pull in the light and occasional buyers, which is where the growth lives. Four, duplication of purchase: brands share buyers with their rivals in line with size, because people buy from a repertoire. Five, mental and physical availability: be easy to think of, through distinctive assets, and easy to find, through distribution and the shelf. Six, penetration, not loyalty: almost all growth comes from adding buyers, not from squeezing the ones you already have. Seven, build long and activate short, on roughly a 60/40 split, because brand building drives most of the growth. Together they say the same thing. Growth is reach and availability, not devotion.

So the useful question is not how to make people love you more. It is why, knowing all this, the industry spends as if the opposite were true.

If loyalty is such a weak lever, why is most of your money chasing it?

Look at where the money actually goes. In a 2026 survey of three thousand marketers, brand owners reported putting more than half of their total marketing budget, about 51 percent, into loyalty and customer relationship management [4]. Spending on retail media, the advertising you buy from retailers to reach shoppers, has climbed to around a fifth of some consumer-goods advertising budgets and is built almost entirely on first-party data, which means it concentrates on people already buying in the category [5]. The brand-building half of the budget, the part that reaches new buyers, has been quietly shrinking for a decade. The money is pouring toward the buyers you already have.

Why, when the evidence points the other way? Not because anyone is stupid. Because loyalty and targeting are measurable, and reach is not. When you email your loyalty base or retarget a recent shopper, you can draw a clean line from the spend to a sale and put it in a deck. When you run a broad campaign that makes a hundred thousand people who have never bought you a little more likely to pick you up next year, the payback is real but slow and hard to attribute. Faced with a chief financial officer who wants a number this quarter, the manager spends where the number is easy. The loyalty-tech paradox is not a failure of intelligence so much as a failure of measurement dressed up as strategy.

There is a trap inside the trap, and it is worth separating cleanly. A loyalty programme is two things at once: a frequency engine, which the evidence says works far less than claimed, and a data asset, which can be genuinely valuable for insight and measurement. The mistake is funding the first while quietly relying on the second to justify it. If the real prize is the data, defend the spend on the data, and do not pretend it is buying loyalty it will not deliver.

Mental and physical availability. Two simple ideas explain most of growth. Mental availability is how easily your brand comes to mind in a buying moment, built from distinctive assets (the colour, the logo, the jingle you own) and from being linked to many "category entry points", the little cues like "quick midweek dinner" or "something for the kids". Physical availability is how easy you are to actually find and buy: in distribution, on the shelf, at eye level, in stock. Get both high and you are easy to buy. Neither is about love.

What are you actually buying when you buy loyalty?

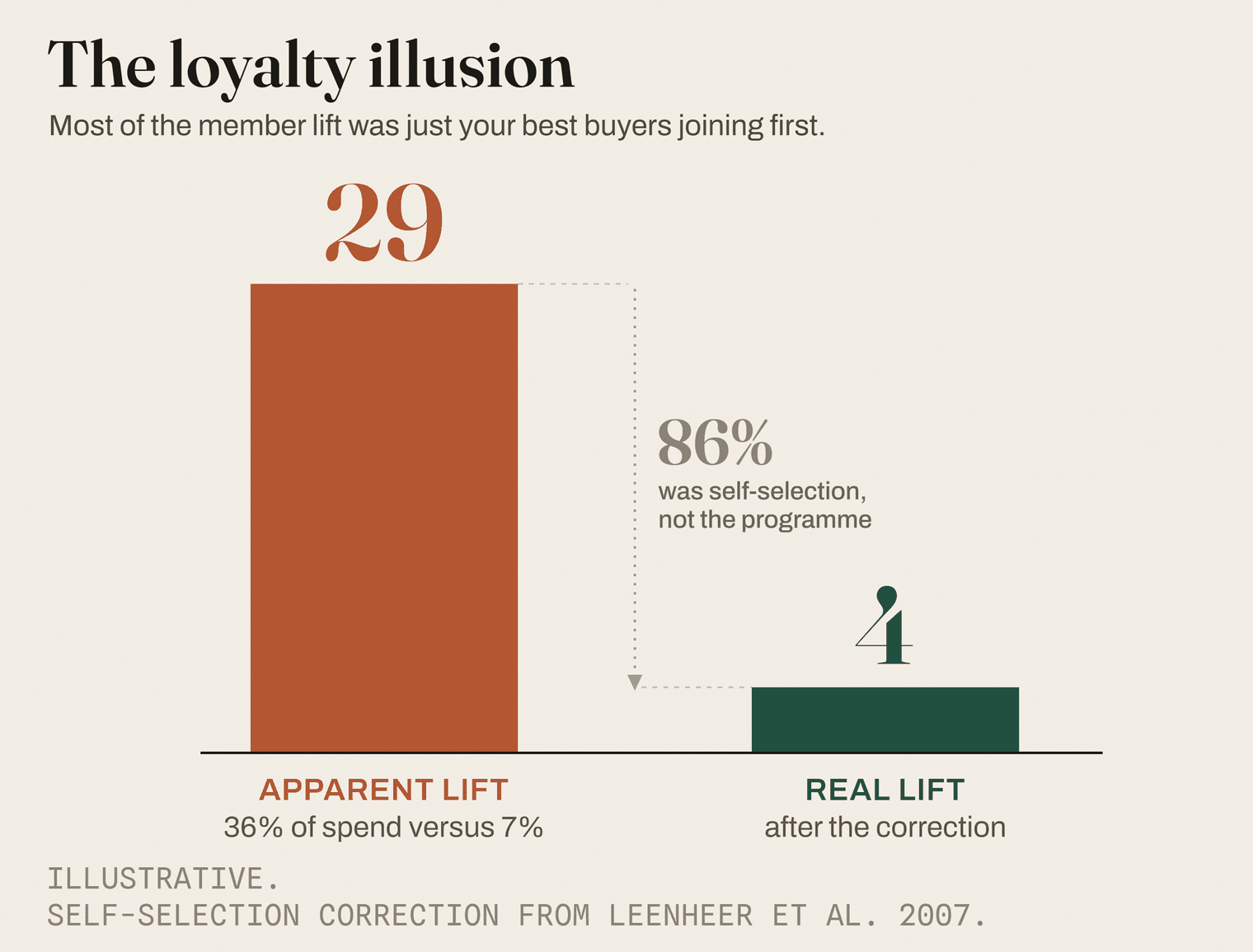

Here is the number that should reset every loyalty business case. When researchers studied grocery loyalty programmes, members looked dramatically more valuable than non-members: members gave the retailer about 36 percent of their category spend against just 7 percent for non-members, an apparent 29-point lift [6]. Run that through a spreadsheet and any programme looks like a triumph. Then they corrected for the obvious problem, that your heaviest, most loyal shoppers are the ones who sign up in the first place. Once you strip out that self-selection, about 86 percent of the apparent advantage disappears [6]. The programme did not create most of that loyalty. It enrolled it.

The loyalty self-selection correction. Why do members look so much more loyal than non-members? Mostly because your best customers join first. They were already buying you heavily, then they signed the card, and now the card takes the credit. The real test of a programme is not the gap between members and non-members. It is what a member does after joining versus what they would have done anyway. On that test, the real lift is a small fraction of what the dashboard shows.

I want to be fair to the other side, because the evidence is not one study. A forty-year meta-analysis of more than four hundred findings concludes that loyalty programmes do help, conditionally, and that the clearest gains come from nudging light and moderate buyers rather than rewarding heavy ones [7]. That is an important nuance, and notice what it actually says: programmes earn their keep when they convert occasional buyers into slightly more regular ones, which is penetration-adjacent work, not when they shower points on the devoted. The problem is not loyalty programmes in principle. It is the business case that promises a 30-point lift from a scheme that, by design, signs up the people who were never going to leave.

And there is a floor you cannot ignore. Penetration is a leaky bucket, so you do lose buyers every year and you do have to replace them. But a bucket that leaks badly is usually telling you something else is wrong, that you have slipped out of distribution, or the product has stopped being good. Fix the hole with availability and quality before you bolt on a programme to bail water.

Walk the money through. (These figures are illustrative; the correction behind them is sourced.)

A category buyer spends 200 pounds a year in your category. Your members appear to give you 36 percent of that, 72 pounds, against 7 percent, 14 pounds, from non-members: a 58-pound apparent lift each. Across a million members that is 58 million pounds of "extra" sales, set against, say, a 6-million-pound programme cost. A ten-to-one winner, on paper. Now apply the correction. The real causal lift is closer to 4 points, about 8 pounds a member, 8 million pounds across the base, against the same 6 million pounds of cost plus the margin you hand back in points. The programme that looked like ten-to-one is barely above water, and its real value was never the loyalty. It was the data.

Why does being easy to buy beat being easy to love?

Step outside grocery for a moment, because the cleanest proof of this idea comes from somewhere else entirely. In 2022 a search engine paid a phone maker around 20 billion dollars in a single year for one thing: to be the default in the browser [8]. Not to be better, not to be loved, just to be the option already selected. When a court examined the deal in 2024, it found the default decisive even though switching took only a little effort, and the reason was buried in the search engine's own research: when they had secretly swapped users to a rival, about half did not even notice [8]. People mostly do not choose what they love; they take what is already in front of them. Being the default beat being preferred, and it was worth 20 billion dollars.

The shelf is the same story in miniature. Eye level is the default. The first result in the retailer's app is the default. Being in stock when the shopper is standing there is the default. This is physical availability, and the data says it does more heavy lifting than almost anything else you spend on. In the one rigorous study that measures them side by side, distribution moved sales about six times harder than advertising did [9], and the 2025 read of consumer-goods growth named distribution expansion, not pricing or loyalty, as the single biggest lever separating the winners from everyone else [10]. Mental availability is the other half: brands that are, in Kantar's phrase, "meaningfully different to more people" command up to five times the penetration of brands that are not [11], and the way you get there is distinctive assets and being linked to more of the little moments when someone might buy the category [12].

None of that is about affection. It is about being the easy answer when a half-attentive shopper, in a hurry, reaches for something. Make yourself the easy answer for more people, in more moments, in more places, and you grow. That, in the end, is most of the job.

There is a worked example hiding in your own numbers. (Illustrative again, and it reconciles.)

Say your brand reaches 20 percent of the 100 million people who buy your category, so 20 million buyers, each buying you about four times a year: 80 million packs. The loyalty plan asks all of them to buy 10 percent more often, four times becoming four and a half. The laws say that is brutally hard, because about half of your buyers buy you only once or twice a year and have no intention of changing, but suppose you pull it off: 8 million extra packs. The availability plan goes after the 80 million people who do not buy you at all. Convert just 5 of those 100 points of penetration, 5 million new buyers, and because new buyers are light, buying maybe twice a year, that is 10 million packs. The frequency pool is capped by a law. The penetration pool is the eighty million people currently ignoring you. Same effort, and the bigger, more reachable prize is the one the dashboard never shows you.

The targeting trap: how precision is starving your growth

The defenders of the loyalty-tech spend have one good word on their side: efficiency. Why pay to reach a hundred people when ninety will never buy you? Target the ten. It sounds unarguable, and it is quietly strangling growth. At the 2025 conference of the body that holds the largest database of marketing effectiveness, the headline finding was that the size of your budget explains about 89 percent of the variation in long-term profit payback, while your return-on-investment efficiency explains only about 11 percent [13]. In other words, reaching enough people matters roughly eight times more than squeezing each pound. And what are marketers doing? The same study found 56 percent of them narrowing their targeting to sub-segments, and 62 percent no longer aiming at the over-45s at all [13]. The body running the study called the trajectory a "death spiral".

The budgets have followed. The long-running benchmark says brands should split roughly 60 percent of spend to long-term brand building, the broad campaigns that create future demand among people who do not buy you yet, and 40 to short-term activation, the promotions and performance ads that harvest demand that already exists; by 2024 the real-world ratio had inverted to about 31 percent brand and 69 percent performance, and the analysis found that rebalancing back toward brand lifted revenue return by a median of about 90 percent [14][15]. The industry moved away from the optimum precisely as the evidence for it hardened.

I should be careful here, because the smartest pushback is real. Reach does not mean blunt, mindless mass. An Oxford study of more than a thousand campaigns found that optimising for raw reach alone delivered weak results, low single-digit business lift, while a smartly built mix of channels delivered fifteen to eighteen percent [16]. The lesson is not "spray and pray". It is reach the whole category cleverly, the light buyers and the non-buyers as well as the heavy ones, rather than narrowing onto the few you can already see. And there is one important exception: a genuine challenger with a tiny budget may be right to start with activation, because it has no base to defend yet. The inversion is a problem for the established brand with a real franchise, which is most of the money in the room.

The targeting trap also explains a quiet irony in the last two issues of this newsletter. Retail media, the booming business of buying ads from retailers, is sold as precision, but it runs on the retailer's record of who already buys, so it mostly reaches people in the category already; on one large platform only about a third of the sales it claimed were genuinely new to the brand [17]. Private label, meanwhile, wins on pure physical availability: the retailer owns the shelf, so its own brand is always in stock, always in front of you, the easiest thing to buy in the aisle. Both are really about availability, not the precision they are sold as.

So when is loyalty actually the right game?

If I only argued one side of this, I would be doing exactly what I have just criticised. There are real situations where retention is the main event, and a good operator names them rather than pretending they do not exist.

The clearest is the subscription or direct-to-consumer model. When the customer signs up and pays every month, keeping them is the business, and the maths of customer lifetime value against acquisition cost is the right maths. Even the penetration school agrees: in subscription markets, growth is recruiting new subscribers while the loyalty lever is simply how many of them stay. The second is the mature category almost everyone already buys, where there is little penetration runway left, so the lever shifts to selling more, trading people up, and improving mix. The third is the identity and prestige category, where the product carries meaning and switching costs are real, and a measure of genuine devotion exists that an everyday biscuit will never command. The fourth is defensive: where almost every competitor runs a programme, a study across 27 countries found the sales benefit of having one all but vanishes, which means you may have to run yours simply to stop losing share, even though it grows nothing [18]. That is a tax, not an engine, and you should book it as one.

Which game are you in? Four quick questions. Is your category one people buy from a repertoire of brands, or one they subscribe to and stay? Is there a long runway of people who do not buy you yet, or are you near the ceiling of category buyers? Is the purchase routine and low-attention, or wrapped in identity and meaning? And are you the only one with a programme, or is everyone running one? Repertoire, runway, routine, and a crowded field all point to availability. Subscription, ceiling, identity, and a lone programme are where retention earns its keep.

The most useful proof that you cannot love your way to growth comes from the brands that tried hardest. The celebrated direct-to-consumer names of the last decade were built on community and devotion, and almost all of them hit the same wall. One eyewear brand now takes roughly 70 percent of its revenue through physical stores it once swore it would never open [19]. A beauty brand that defined online-native cool found its breakout year when it finally walked into a national retail chain [20]. A razor subscription that became a case study in loyalty was eventually sold by its parent, whose leaders conceded that acquiring a customer online cost about the same as in a shop but reached far fewer people [21]. Love was a wonderful asset, but it was never a substitute for being easy to buy.

Is this just "spend more on advertising"?

No, and the difference matters. The argument is not "advertise more". It is "stop pointing your money at the people you already have". You can act on that without spending an extra pound, by moving budget from retargeting your base to reaching the category, from the loyalty programme's frequency promises to the genuine work it can do as a data asset, and above all from chasing love to fixing availability, the distribution gaps, the out-of-stocks, the missing pack at the magic price, the distinctive assets you have let fade. Easy to buy is mostly an allocation decision, not a bigger cheque.

The pushback I expect. Let me take the three I hear most, head on. "But the studies show loyalty programmes work." They help conditionally, mostly by nudging light buyers toward becoming regular ones, which is penetration work; the trap is the business case that projects a 30-point lift from a scheme that signs up your most loyal buyers first. "We need the first-party data." Then justify the spend on the data and the measurement, which are real, and stop crediting it with a frequency lift it will not deliver. "If we drop our programme our rivals will take our share." Where everyone runs one, that is true, so treat the programme as a defensive cost and stop calling it growth.

What would change my mind. I would accept I am wrong on either of two specific tests. First, if across a broad set of everyday categories the brands that put the highest share of spend into loyalty and targeting turn out to grow their buyer base faster than comparable brands that spend it on reaching the category, through 2027. Second, if a brand in a low-penetration category, with no dominant programme, shifts twenty points of budget from loyalty and retargeting into broad reach for two years and fails to add buyers, while its loyalty metrics climb on their own. Either result would tell me availability is not the lever I think it is. I will be watching both.

For now the weight of the evidence points one way, and it has for years. Your buyers are not waiting to love you more. There are tens of millions of people who simply find you a little too hard to think of, or a little too hard to find, and they are where your growth lives. Spend the next planning round making yourself easier to buy, not easier to love, and you will have the laws of growth on your side for once, instead of fighting them.

Signals

- About 80 percent of brands that grew worldwide did so by adding buyers, not by lifting frequency, rising to 88 percent in Asia (Kantar Brand Footprint, 2025): https://www.kantar.com/inspiration/fmcg/brand-footprint-2025-asia-remains-an-fmcg-growth-hotspot

- Marketers now put about 51 percent of total marketing budget into loyalty and customer relationship management, a self-reported industry survey of 3,000 marketers (Antavo, 2026): https://antavo.com/news/antavo-gclr-2026-report/

- At the 2025 effectiveness conference, budget size explained about 89 percent of profit payback and return on investment only about 11 percent, with most marketers narrowing their targeting (IPA, 2025): https://ipa.co.uk/news/go-big-or-go-home

- A search engine paid around 20 billion dollars in one year to remain the default in a browser, and a 2024 antitrust ruling found the default decisive (United States v. Google, 2024): https://9to5mac.com/2024/08/05/googles-20b-default-search-deal-with-apple-violates-antitrust-law-judge-rules/

- A leading direct-to-consumer eyewear brand now takes about 70 percent of its revenue through physical stores (Retail TouchPoints, 2024): https://www.retailtouchpoints.com/topics/omnichannel-alignment/a-financial-tale-of-two-former-dtc-darlings-allbirds-and-warby-parker

References

- Kantar, Brand Footprint 2025 (growth through penetration; Asia and China figures). https://www.kantar.com/inspiration/fmcg/brand-footprint-2025-asia-remains-an-fmcg-growth-hotspot

- Ehrenberg-Bass Institute, How Categories Grow (Dunn and others), Journal of Business Research, 2025 (penetration tracks revenue; frequency is stable). https://www.sciencedirect.com/science/article/pii/S0148296325002085

- Byron Sharp, How Brands Grow, Oxford University Press, 2010 (double jeopardy; the Pareto 60/20; the Coca-Cola buyer profile, page 41). https://global.oup.com/academic/product/how-brands-grow-9780195573565

- Antavo, Global Customer Loyalty Report 2026 (self-reported survey of 3,000 marketers). https://antavo.com/news/antavo-gclr-2026-report/

- eMarketer, retail media advertising forecast and trends, 2025. https://content-na1.emarketer.com/retail-media-ad-spending-forecast-trends-h2-2025

- Leenheer and others, the effect of loyalty programmes on share of wallet, International Journal of Research in Marketing, 2007 (self-selection correction), as reported in Ziliani and Ieva, 2019. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=969532

- Belli and others, a meta-analysis of loyalty programme effectiveness, Journal of the Academy of Marketing Science, 2022. https://link.springer.com/article/10.1007/s11747-021-00804-z

- United States v. Google, ruling of August 2024, and the reported 20 billion dollar default-search payment. https://9to5mac.com/2024/08/05/googles-20b-default-search-deal-with-apple-violates-antitrust-law-judge-rules/

- Friberg and Sanctuary, the effect of retail distribution on sales, Marketing Science, 2017 (distribution elasticity about six times advertising, Swedish market). https://doi.org/10.1287/mksc.2017.1038

- Circana, 2025 US CPG Growth Leaders, April 2026 (distribution expansion as the leading growth lever). https://www.globenewswire.com/news-release/2026/04/09/3271056/0/en/Circana-Announces-2025-U-S-CPG-Growth-Leaders.html

- Kantar, Blueprint for Brand Growth, 2024 (meaningfully different brands command up to five times the penetration). https://www.kantar.com/campaigns/blueprint-for-brand-growth

- Jenni Romaniuk, Ehrenberg-Bass Institute, on distinctive assets and category entry points. https://marketingscience.info/

- Les Binet and James Davis, "Go Big or Go Home", IPA Effectiveness Conference, 2025 (budget explains 89 percent of payback; the targeting "death spiral"). https://ipa.co.uk/news/go-big-or-go-home

- Les Binet and Peter Field, The Long and the Short of It and Effectiveness in Context, IPA (the 60/40 split; loyalty versus acquisition effect rates). https://ipa.co.uk/knowledge/effectiveness-research-analysis/les-binet-peter-field

- WARC, The Multiplier Effect, 2024 (the 31:69 actual split; the revenue uplift from rebalancing). https://www.warc.com/the-multiplier-effect

- Felipe Thomaz, University of Oxford, analysis of more than 1,000 campaigns on reach and channel mix, 2024. https://www.mi-3.com.au/03-07-2025/6040-rule-losing-relevance-especially-challenger-brands

- Tinuiti via Dataslayer, retail-media new-to-brand share, 2025. https://www.dataslayer.ai/blog/incrementality-becomes-the-primary-kpi-for-retail-media-advertisers

- Bombaij and Dekimpe, do loyalty programmes work across countries, 2020 (the effect fades where most competitors also run one). https://loyaltyrewardco.com/do-loyalty-programs-work-a-review-of-scientific-evidence/

- Retail TouchPoints, the physical-store turn at two former direct-to-consumer brands, 2024. https://www.retailtouchpoints.com/topics/omnichannel-alignment/a-financial-tale-of-two-former-dtc-darlings-allbirds-and-warby-parker

- WWD, a beauty brand's retail breakout, 2024. https://wwd.com/beauty-industry-news/beauty-features/glossier-talks-numbers-sephora-1235880069/

- Digital Commerce 360, the sale of a razor subscription business, 2023. https://www.digitalcommerce360.com/2023/10/30/unilever-is-selling-dollar-shave-club-after-seven-years/