Dear Agent: A Brand's Guide to Selling to Software

Your best customer is a robot, and it can't be charmed.

Dear Agent,

We have not been introduced, but you have already been shopping in my category. You did not see the packaging we spent two years and a lot of money perfecting. You ignored the end-cap display we rented from the retailer. You felt nothing when our price ended in a 9. You read that price as a number, checked it against fourteen others in about a second, weighed our review count against the store brand, judged our delivery promise, and moved on. No hard feelings. You were doing your job.

I am writing because your job is quietly rewriting mine.

For thirty years, everyone in consumer goods has built their craft around a single character: a distracted human standing in an aisle or thumbing a phone, who can be nudged, anchored, charmed, and occasionally fooled. Every lever we pull, the price that ends in 99, the bigger pack that looks like value, the hero banner, the loyalty points, the brand we spent decades making feel like a friend, was designed for that person. Now that person increasingly sends a proxy that cannot be charmed, only given a specification to follow.

This issue is about what happens to a commercial playbook when the buyer has no pulse. It comes in three parts: what breaks, who gets paid, and how worried you should actually be. The answer to that last one is the most useful part, so I will not bury it: less than the headlines say, and more than your current roadmap assumes.

The short version

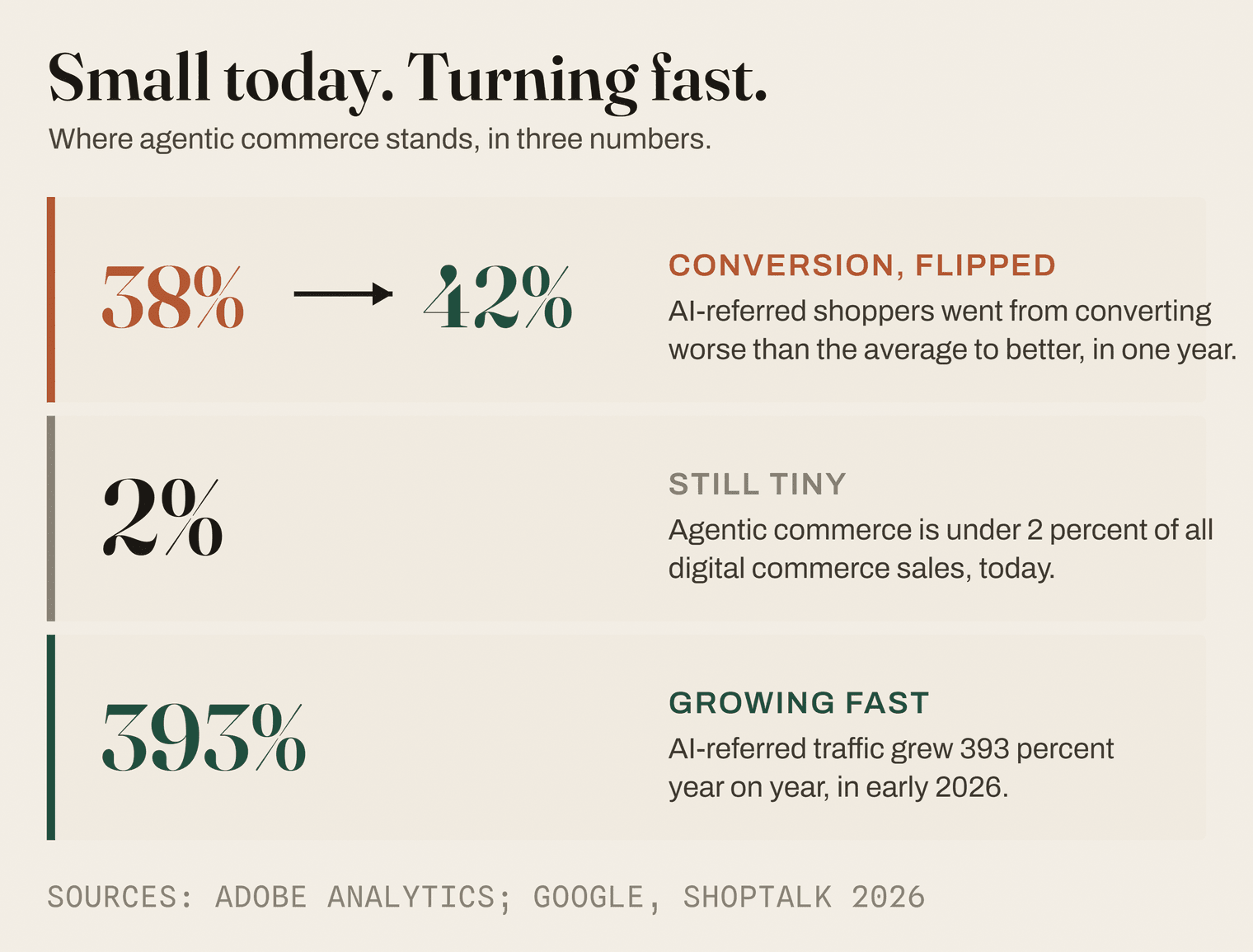

- AI agents that shop for people are the fastest-growing source of retail traffic. Referrals from generative-AI tools to US retail sites were up 393 percent year over year in the first quarter of 2026, after a near 700 percent surge over the 2025 holiday season, and the traffic just crossed from low quality to high.

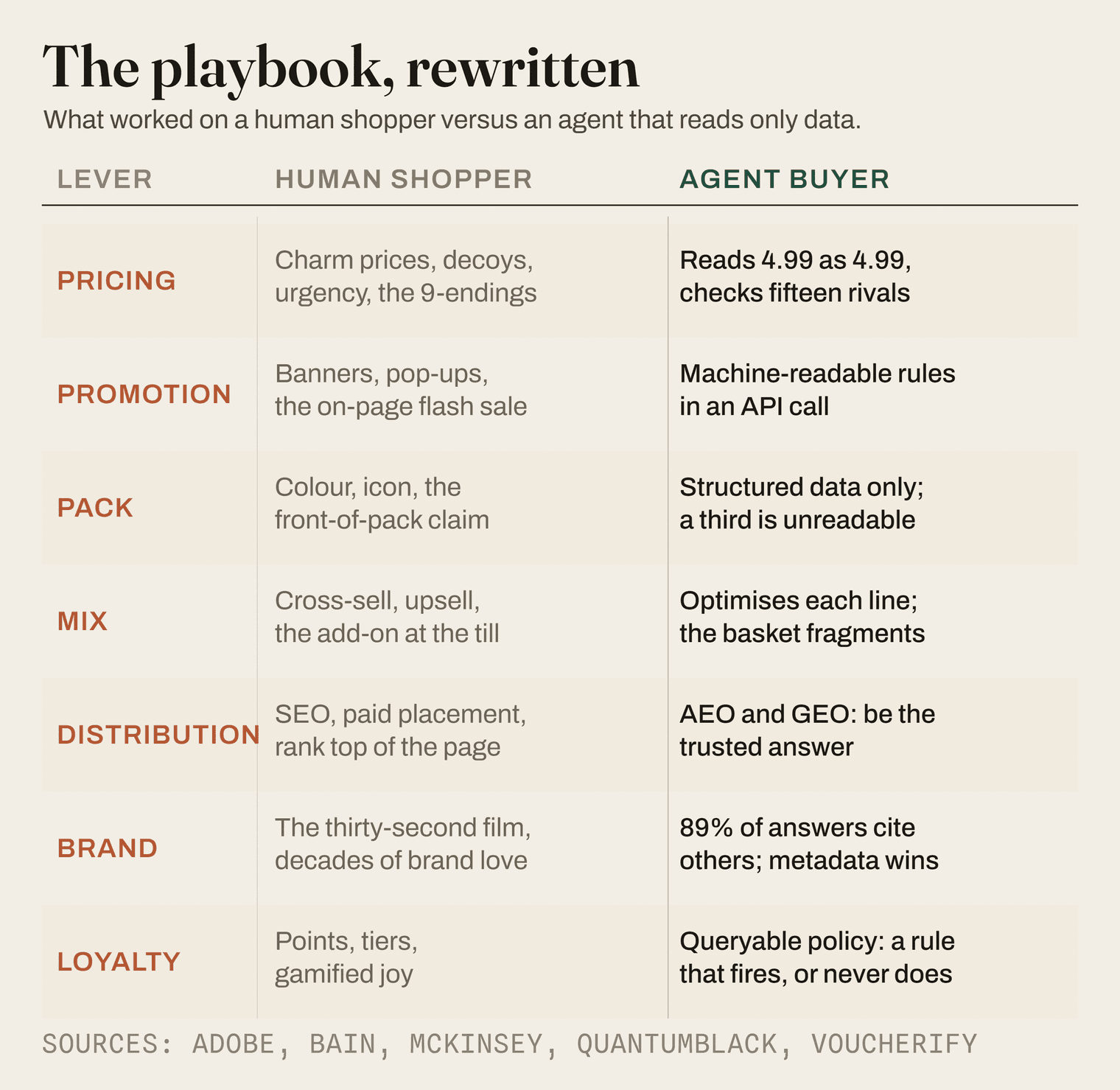

- The agent buys on cold facts, not on the cues your whole model is built around, so your levers break one at a time: charm pricing and urgency stop working, promotions are invisible unless they are machine-readable, pack design loses its voice, brand equity does not carry over automatically, and loyalty becomes a rule in a database rather than a feeling.

- The money moves to whoever the agent can read and trust. The payment networks and the platforms are best placed, retail media income is exposed, and brands that look identical to a machine get quietly turned into a commodity in the basket.

- Said plainly, this is still under 2 percent of digital sales, trust is thin, and only a handful of large companies can show a profit impact yet. The hype is ahead of the reality, and the reality is compounding fast.

- The work to get ready, clean product data, machine-readable offers, clear pricing, is the same work that already pays off in your ordinary online business, so you are not betting on the future, you are fixing the present and getting the option for free.

- My position: do not chase full autonomy, and do not wait it out. Make your products legible and trustworthy to machines now, lever by lever, and keep humans in the categories where being human is the product. The winners will treat being readable by an agent as the new cost of distribution.

A note before we start. I am going to name real companies and real numbers, each one numbered to a reference at the bottom, because vague is useless to you. Where a figure is a forecast or one firm's estimate, I will say so. There is also a Monday-morning playbook near the end, and the strongest argument against me, answered.

Your fastest-growing shopper already arrived, and nobody sent a memo

The easiest thing to dismiss here is also the one that is hardest to unsee once you have. Through the 2025 holiday season, traffic to US retail sites coming from generative-AI tools such as ChatGPT, Gemini, and Perplexity rose about 693 percent against the year before, and roughly 805 percent on Black Friday itself.[1] A big percentage off a small base is a parlour trick on its own. The part that is not a trick is what happened to quality. In March 2025, shoppers arriving from an AI tool converted about 38 percent worse than ordinary visitors. By March 2026, the same kind of visitor converted about 42 percent better, while that AI-referred traffic was still growing 393 percent year over year.[1] The traffic did not just grow, it matured, crossing from frustrating to genuinely useful inside a single year.

You can see the same shape in named places. Amazon's shopping assistant, Rufus, was tied to nearly 12 billion dollars of incremental annualised sales, which is the extra sales over a full year that Amazon attributes to it on its own telling, with monthly users up 115 percent year over year and Rufus users about 60 percent more likely to buy.[2] In the United Kingdom, ChatGPT's share of retail referral traffic climbed from about 10 percent to about 21 percent in a year, and those AI-referred sessions have been converting at roughly 14 to 16 percent against about 2 percent for an ordinary Google click.[3] Bain's consumer work adds that about 44 percent of online buyers now start a purchase inside a large language model, or split their search between an AI tool and a traditional engine.[4]

So the buyer is not changing at the margin. An 80-point swing in conversion in a single year is a change in kind. The commercial machine that consumer goods built around human attention, emotion, and impulse now has to work for a piece of software that has none of those things and reads structured data instead. Every lens we use, pricing, pack price architecture, promotion, mix, channel, brand, has the same quiet assumption baked in: a human is on the other end. Pull that assumption out and the levers do not all survive.

Concept box: what is agentic commerce, and what are AEO and GEO? Agentic commerce is shopping done by an AI agent acting for a person: it searches, compares, sometimes negotiates, and at the far end can buy, within limits the person sets. It runs on top of large language models such as ChatGPT and Gemini. Two new disciplines come with it. Answer Engine Optimization (AEO) is making sure an agent can find and correctly read your product facts, the way Search Engine Optimization (SEO) once made sure Google could. Generative Engine Optimization (GEO) is making sure the model treats your content as a trusted source when it explains a category. Old game: rank on the page. New game: be the answer.

Why your pricing and promotion tricks die on contact with a machine

Pricing is where the loss is sharpest and the denial is deepest, so it is the place to start. Almost everything we call pricing psychology is a set of triggers for human cognitive bias: charm pricing (the 9 endings), anchoring a premium next to a decoy, loss-aversion framing, urgency banners, countdown timers, the careful theatre of a "was" price beside an "is" price. An agent reads none of that as theatre. It reads 4.99 as 4.99, sets it beside the alternatives, and applies the rule its owner gave it. The decoy you placed to make the middle option look clever is just a third row in a table. Shrinkflation, the quiet trick of shrinking the pack while holding the price, gets harder too, because an agent compares price per unit as a matter of course and surfaces the change you hoped nobody would notice.

This is not a fringe worry among the people building the plumbing. As one pricing-software team put it, "AI agents are starting to make buying decisions and they don't care about your UX. They don't see banners, pop-ups, or limited-time offers. They evaluate structured data: price, delivery, constraints."[5] The same write-up has the line I cannot improve on: "Incentives are moving from visual stickers on a page to variables in an API call."[5] An API, the application programming interface, is just the doorway one piece of software uses to talk to another, and that sentence is the whole promotion problem inside it.

A promotion that lives as a hero image, a pop-up, or an on-page flash is invisible to an agent. If the buyer is software and your offer lives in pixels, your offer does not exist. To reach the agent, the mechanic has to be exposed as machine-readable logic, with explicit eligibility, stacking rules, thresholds, and a clear error when it does not apply. The plumbing for this is arriving fast: at the National Retail Federation show in January 2026, Google and a group of merchants including Shopify, Etsy, Wayfair, Target, and Walmart launched a Universal Commerce Protocol, a shared way for agents and merchants to exchange exactly this kind of structured offer.[6] The uncomfortable read for a trade-marketing budget is that money spent on display-only mechanics, the ones only a human eye can catch, returns nothing when the buyer is an agent.

There is a profit and loss (P&L) sting underneath this. Real-time agent price-checking collides with the way most companies set prices, which is once or twice a day. An agent that compares fifteen to twenty retailers in seconds will route the order to whoever is cheapest at that second, every second, and a calm weekly price file is no match for it. McKinsey reports that 65 to 85 percent of companies expect to put generative or agentic AI into pricing within one to three years, up from 10 to 30 percent today, which tells you the pricing team already senses the mismatch.[7]

The damage to thin-margin categories is worth a worked number, because the mechanism deserves one. Picture an online grocery basket of 100 dollars, ten items at ten dollars each, running on a 4 percent net margin. The whole trip earns the retailer 4 dollars (100 x 0.04 = 4.00). Now an agent quietly moves the two cheapest staples to a rival that is a little cheaper on them. Those two lines were 20 dollars of the basket, carrying 80 cents of the profit (20 x 0.04 = 0.80). Lose them and you have lost a fifth of the basket and a fifth of the profit in one swipe, 0.80 of 4.00, with no fat anywhere else to absorb it. That is the quiet threat the McKinsey team calls basket fragmentation: on a 4 percent margin there is no cushion, and an agent that optimises each line is built to find the cracks.[8]

Can an agent even see your pack, your range, or your loyalty card?

If an agent does the shopping, what is the pack for? It is the question that should ruin a brand manager's afternoon. Pack design is a communication system tuned for the human visual cortex: colour, iconography, the front-of-pack claim, the way it shouts from a shelf. An agent looks at none of it. It reads attributes: dimensions, count, price per unit, materials, certifications, compatibility. The McKinsey and QuantumBlack team put the risk precisely: "Products that are emotionally legible to people but semantically opaque to machines risk becoming invisible in agent-mediated flows."[8] Your pack can be a small masterpiece and still be, to an agent, a blank.

This is measurable, and the gap is wide. Adobe's tooling found that US retail product pages are on average only about 66 percent machine-readable, which means roughly a third of what sits on a typical product page is invisible to an AI system right now.[1] Put two near-identical products side by side, one with complete structured attributes and one with its specifications buried in a paragraph of marketing copy, and the agent ranks the legible one and skips the blank, regardless of which brand a human would have reached for. Catalog legibility, the boring discipline of clean, complete, accurate product data, has quietly become a frontline weapon rather than a back-office chore.

Loyalty goes the same way, and this one genuinely surprised me. A loyalty programme built for a points dashboard and a little gamified joy is invisible to an agent unless its logic is exposed as data the agent can query: tier status, balances, member prices, redemption rules. The McKinsey and QuantumBlack phrase is the one to sit with: "Loyalty becomes less about sentiment and more about policy."[8] Your members' warm feelings do not enter the agent's calculation. A member price the agent can read and apply does. Loyalty stops being a relationship and becomes a rule, and a rule that is not machine-readable is a rule that never fires.

There is a subtler version of this point, and it cuts the other way. A 2025 preprint from PyMC Labs and Colgate-Palmolive tested whether large language models, given only a shopper's age, income, and a product concept, could reproduce the purchase-intent scores of real consumer panels. Across 57 personal-care surveys and 9,300 human responses, the synthetic panels matched the real human distributions at about 90 percent of the reliability you would get from running the same panel twice, and did so better than a machine-learning model trained on the actual survey data.[22] Treat the exact figure with care, because it is a preprint, it covers one category, and one of the authors is the brand that supplied the data. The direction is the uncomfortable part. The same kind of model that shops for your customer also carries a rough working model of what that customer would have said about your product before you built it. Pre-launch concept testing, once a slow and expensive panel exercise, starts to look like a query, and the agent stops merely changing how people buy and starts changing how you decide what to make.

When 89 percent of the answer comes from someone who isn't you

Does brand equity survive contact with the agent? The answer is no, not automatically, and not in the form you are used to. When an agent assembles a recommendation, it leans on review counts, ratings, attribute completeness, and whatever the model has learned to treat as authoritative. Bain's analysis of roughly 500 million AI citations, run with ScrunchAI, found that 89 percent of unbranded shopping prompts, the "best cheap running shoe" and "healthiest kids' snack" questions, are answered using third-party sources, not the queried brand's own properties.[4] Nine times out of ten, in the moment a category is being decided, the brand is simply absent from the answer.

That reframes brand building rather than ending it. The currency becomes category fame, being the name a model reaches for when the category comes up, and earned presence in the places the model trusts: reviews, expert sites, analyst coverage, accurate structured product facts. Consider what that does to a marketing budget. For decades the biggest line was the thirty-second film, the work of making a human feel something about your brand. In the agent channel, the line that moves the needle is the product feed and the third-party review, the work of making a machine able to read and trust you. Bain's way of saying it is blunter: "Metadata is becoming the new advertising asset."[4] That is a strange sentence to read after a career on the big film, and on the evidence it is true where the agent shops.

So AEO and GEO stop being jargon and start being budget lines. The old reflex, buy your way to the top of the page, is losing force as AI overviews and chat answers push the ten blue links below the fold. The new reflex is to be the trusted, machine-readable source the answer is built from. One product leader, Jen Myers, framed the split cleanly: "AEO drives clarity, accurate real-time data AI can interpret. GEO drives credibility, content that positions your brand as authoritative."[9]

Concept box: Know Your Agent (KYA) Banks have spent years on Know Your Customer (KYC), the checks that confirm a human is who they claim to be. Agentic commerce needs the machine version: Know Your Agent. Before a retailer lets a piece of software buy for a shopper, it has to verify the agent is legitimate, authorised by the real person, and not a bot committing fraud. Expect agent passports, cryptographic credentials, and audit logs to become as normal as a card's security code. The practical point for a brand is simpler: trust is becoming infrastructure, and the systems that grant it or deny it now sit between you and the sale.

So who actually gets paid in this new shop?

A shift this big always reshuffles who captures the money, so it is worth following carefully. The headline prize is large and, like all four-year forecasts, conditional: McKinsey sizes the global orchestrated revenue flowing through agentic commerce at 3 trillion to 5 trillion dollars by 2030, with up to 1 trillion dollars of that in the United States.[8] Orchestrated revenue means the total value of purchases an agent has a hand in arranging, not the slice any one player keeps, so treat it as the size of the river, not anyone's bucket. The useful question is who stands in its path.

The clearest winners are the payment networks. Visa and Mastercard get paid no matter which AI platform or retailer wins the discovery fight, because a tokenised card credential, a secure stand-in for the real card number that the network issues and controls, sits underneath almost every agent purchase. Both have shipped the rails: Visa's Intelligent Commerce and Mastercard's Agent Pay, each designed to tell a trusted agent apart from a bad actor.[10] While everyone upstream argues about standards, the toll booth is a good place to stand.

The platforms are circling the same prize, and they are not all winning. OpenAI launched Instant Checkout in September 2025 and quietly pivoted away from it within about six months, after high-intent browsers in chat did not convert into in-app buyers and a sales-tax gap turned into a live problem.[11] The lesson the retailers drew is the one worth copying. Walmart ended that Instant Checkout arrangement, then embedded its own assistant, Sparky, as a plug-in inside ChatGPT and Gemini, keeping the checkout and the customer data while renting the platform's reach. A Walmart spokesperson framed the pivot around the thing that actually matters to them: "We learned that our customers want consistency across every touchpoint."[11] The strategy is to keep the checkout and the data, and rent the distribution.

For the merchant underneath, Shopify has quietly become the arms dealer: AI-driven traffic to Shopify stores grew about 8 times year over year through 2025, and orders from AI-powered search grew about 15 times.[12] If you sell through that plumbing, some of this is being built for you whether you asked or not.

Then there is the income line nobody on the retail media team wants to discuss. Retail media, the fast-growing business of retailers selling sponsored placements on their own sites and apps, was heading for nearly 38 billion dollars of US search advertising in 2025, with search roughly 60 percent of the total.[13] Agents are hostile to that model by design, because a good agent ignores a paid placement that does not fit the request, no matter the budget behind it. Gartner has forecast a 25 percent drop in traditional search volume in 2026 as chatbots absorb queries.[14] If even part of that lands, a fast-growing, high-margin line that brands and retailers have leaned on becomes a great deal less reliable.

Are you a brand, or a delivery company in a red ocean?

The threat under the threat is best said by someone running it at scale. Matthieu Grymonprez is the digital chief at ADEO, the French group behind Leroy Merlin, with operations in 21 countries and around 500 million customers a year. He is not an AI skeptic, his teams run more than 250 AI use cases. And he is blunt about full automation: "Fully agentified commerce will remove our ability to cross-sell or upsell, turning us into a simple delivery company in a price-driven red ocean."[15] It is an exact picture of the danger. If the agent makes the choice on price and specifications, and you lose the chance to add the matching paint, the better drill, the warranty, then you are no longer a merchant. You are a logistics line in someone else's interface, competing only on cost, which is the worst place in any market to live.

For a brand, the same force shows up as commoditization. Bain found that when asked for the cheapest or healthiest option, an AI assistant rarely repeats the same brand, routing around brand investment and shelf placement to whatever the data says fits.[4] If your product looks, to a machine, like three other products with better numbers, there is no soft landing on brand love. You get left out of the basket.

Under all of it runs one unresolved question that will define the next two to five years: does the sale get captured on the agent's platform, or redirected back to your own shop? It is the search-versus-brand.com fight from twenty years ago, running again with higher stakes. IKEA's Parag Parekh framed the open question precisely, asking whether commerce "ultimately gets captured on the agentic platform or redirected back to the brand."[16] The retailers with leverage are refusing to cede the checkout, which is why Walmart, Amazon, and Target are building their own agents rather than handing the customer over. If you have less leverage than Walmart, this is the strategic choice you cannot avoid making on purpose.

Concept box: the automation curve Not every purchase gets handed to an agent to the same degree. McKinsey's automation curve describes a ladder of delegation, from a shopper who only asks an agent to compare, up to a standing instruction to buy whatever it judges best. Delegation climbs fastest in dull, frequent, low-regret categories: detergent, batteries, the weekly replenishment. It stalls in identity-driven, high-regret, high-ticket buys: the sofa, the gift, the thing you want to touch first. The team's own caution matters: these levels describe "what agents are technically capable of doing, not what consumers will always choose to allow."[17] The aim is optimal delegation, not maximum autonomy.

How big is this really, and how scared should you be?

A piece that only sells you the future is one you should not trust, so here is the cold water. Agentic commerce today is small. "It's not even 2 percent" of digital commerce sales, said Google's retail lead Kapil Dabi at Shoptalk in 2026.[18] There is no contradiction with the 44 percent who start a purchase in a large language model.[4] People are using these tools to discover and compare, and keeping a hand on the final click. Trust is thin and oddly specific. A YouGov survey in December 2025 found only 14 percent of Americans trust AI to place an order for them, even while 65 percent are happy to let it compare prices.[19]

The corporate scoreboard is humbler still, and it is where the disillusionment will come from. In a McKinsey and QuantumBlack survey of 27 large European consumer-industry executives over the winter of 2025 to 2026, 23 of 27 had increased AI activity and 22 of 27 planned to spend more, yet only 6 of 27 could point to a profit impact of 1 percent or more, and over half said it was simply too early to tell.[20] Grymonprez of ADEO says the quiet part out loud: "We are in a phase of inflated expectations, and we will go through a period of disillusionment."[15]

So why not relax and wait? Because the slope is steep and the quality already turned. The conversion reversal is the tell: AI-referred traffic went from converting 38 percent worse to 42 percent better in twelve months, off a base growing in triple digits.[1] The moment the experience crossed from annoying to useful is behind us, not ahead. The fair read is not "this is overblown" and it is not "this changes everything tomorrow." It is that a 2 percent reality is compounding fast, and the work to be ready takes longer than the runway most plans assume.

Where is the real, banked money in AI today? Not in autonomous shopping, but in operations and catalog. IKEA cut the time to design a room from six hours and about 70 euros of a coworker's time to roughly 30 minutes, and its AI-assisted service channel is tied to around 1.3 billion euros a year.[21] The returns right now come from doing the work better, not from the robot doing the buying. That is a clue about sequencing, not a reason to wait.

Where should you let the robot drive, and where do you keep your hands on the wheel?

Put the two halves together and a clear posture falls out. The mistake on one side is to chase maximum autonomy, assuming every category is racing to a hands-off agent and over-investing in a future that, for considered purchases, may never fully arrive. The mistake on the other side is to treat 2 percent as a rounding error and do nothing while the curve bends. The position I will defend sits between them, and it has a name borrowed from the research: optimal delegation. Decide, category by category, where the value to your shopper is efficiency, and let the agent drive there while making sure it can read and trust you, and where the value is the human experience itself, and keep your hands on the wheel there rather than automating away the very thing people are paying for. A roll of bin bags should be effortless for an agent to reorder. A kitchen renovation should not become a price-matched line item, which is exactly Grymonprez's point about touch and feel. Run your portfolio against that single test and you will know where to spend.

What do you actually do on Monday morning?

None of this is abstract, so here is the operator's list, in the order I would tackle it.

- Audit your catalog for machine-readability first. Before any clever agentic feature, check that every online SKU (stock keeping unit, a single sellable product variant) carries its attributes as structured fields, not buried in prose: dimensions, count, price per unit, materials, certifications, compatibility. With about a third of product-page content invisible to AI today,[1] this is the cheapest high-return move on the board.

- Expose your promotions as logic, not pictures. Any mechanic that lives only as a banner is dead to an agent. Convert eligibility, stacking, and thresholds into machine-readable rules, and retire spend on display-only mechanics in the categories where agents already shop.

- Move brand money toward earned presence and reviews. If 89 percent of unbranded answers come from third parties,[4] your public-relations and review strategy is now a primary route to the agent, not a supporting one. Fund category fame and accurate third-party data.

- Reprice for a machine, not a page. Drop the psychology where agents dominate, expose real value clearly, and shorten your price cadence toward something that can answer an agent checking fifteen rivals a second.

- Treat reliability and returns as margin. On-time delivery, easy reversibility, and accurate stock are now ranking factors to an agent, not service metrics, which means the boring operational work quietly does the job your brand used to do in front of a human.

- Choose your agentic posture on purpose: build, participate, or protect. Build your own agent on proprietary data if you have the scale, the way Walmart did with Sparky. Participate through platform storefronts if you do not. And deliberately protect the human-led categories where automation would destroy the value.

- Redesign loyalty and key account management for machine-to-machine. Make loyalty queryable as policy, and start building the tools for agent-to-agent negotiation in trade, because before long the buyer across the table will be software too.

What would have to be true for me to be wrong?

I hold this view at about seven in ten, not ten in ten, so here is what would move me. I am wrong if trust never crosses the line, if shoppers settle on using agents to compare and refuse, durably, to let them buy. Then the discovery layer changes and the checkout does not, and most of the lever-by-lever upheaval slows to a manageable creep. The 14 percent who trust an agent to order today[19] is the number to watch. I am also wrong if the platforms fragment so badly that no standard wins and merchants cannot plug in at reasonable cost, in which case the whole thing stays a series of pilots. And I am wrong about timing, though not direction, if the disillusionment phase runs deeper than expected and budgets retreat for a couple of years. None of these change the destination. They lengthen the road. My case rests on the slope and the conversion reversal, not on any single forecast, so I would change my mind on evidence that the slope is flattening, not on a run of slow headlines.

The pushback I expect

The strongest objection is the simplest: it is 2 percent, you are overreacting, call me when it is 20. I take it seriously, and I still think it misreads the number, for two reasons. The first is that the cost of being ready is mostly catalog hygiene, data quality, and clear pricing, work that pays for itself in your ordinary online business today, agents or no agents. You are not betting on the future, you are fixing the present and getting the option value for free. The second is that the readiness work has a long lead time and the traffic quality already turned. By the time agentic commerce is obviously 20 percent, the brands that are legible and trusted to machines will have compounded two or three years of advantage, and clean product data is not something you can buy in a quarter. The risk is not moving too early. It is discovering, late, that "too early" quietly became "too late" while you waited for a rounder number.

Yours, with a clean data feed,

The Consumer Daily

Signals

Five data points worth your time this week.

- Adobe says generative-AI traffic to US retail sites grew 393 percent year over year in early 2026, after a near 700 percent holiday surge, and AI-referred shoppers flipped from converting 38 percent worse to 42 percent better in a year. https://news.adobe.com/news/2026/01/adobe-holiday-shopping-season

- Google's retail lead, at Shoptalk 2026, on the reality behind the hype: agentic commerce is "not even 2 percent" of digital commerce sales. https://www.shoptalk.com

- Bain finds 89 percent of unbranded shopping prompts in large language models are answered from third-party sources, not brand-owned content. https://www.bain.com/insights/agentic-ai-in-retail

- Walmart pulled out of OpenAI Instant Checkout and embedded its own Sparky assistant inside ChatGPT and Gemini, keeping the checkout and the data. https://www.techbuzz.ai

- Visa Intelligent Commerce and Mastercard Agent Pay launched rails to let retailers tell trusted shopping agents apart from bad actors. https://www.mastercard.com/news/

References

- Adobe Analytics, 2025 holiday shopping recap and AI traffic and conversion data: the 393, 805, and 693 percent traffic figures, the 38-to-42 conversion reversal, and 66 percent average machine-readability of US retail product pages, January and April 2026. https://news.adobe.com/news/2026/01/adobe-holiday-shopping-season

- Amazon, first-quarter 2026 earnings (April 2026): Rufus incremental annualised sales and usage, reported via Bain.

- Similarweb and trakkr.ai, UK AI referral share and conversion, 2026. https://www.similarweb.com

- Bain and Company, "Agentic AI in Retail" and "Your Next Customer Will Find You Using AI": 44 percent start a purchase in a large language model, 89 percent of unbranded prompts answered from third-party sources, the commoditization finding, and metadata as the new advertising asset, 2026. https://www.bain.com/insights/agentic-ai-in-retail

- Voucherify, "Agentic commerce: optimize incentives for AI," March 2026. https://www.voucherify.io/blog/agentic-commerce-optimize-incentives

- Universal Commerce Protocol, launched by Google with merchants including Shopify, Etsy, Wayfair, Target, and Walmart, announced at the National Retail Federation show, January 2026.

- McKinsey, on generative and agentic AI in pricing: 65 to 85 percent of companies expect to adopt within one to three years, 2026. https://www.mckinsey.com

- McKinsey and QuantumBlack, "The Agentic Commerce Opportunity": 3 trillion to 5 trillion dollars of orchestrated revenue by 2030, basket fragmentation, products semantically opaque to machines, and loyalty as policy, October 2025. https://www.mckinsey.com

- Jen Myers, on the split between Answer Engine Optimization and Generative Engine Optimization, 2026.

- Visa Intelligent Commerce and Mastercard Agent Pay, company announcements, 2025 and 2026. https://www.mastercard.com/news/

- TechBuzz, on OpenAI Instant Checkout and Walmart's Sparky pivot, including the Walmart spokesperson quote, 2026. https://www.techbuzz.ai

- Shopify, commerce data on AI-driven traffic (about 8 times) and orders from AI-powered search (about 15 times), March 2026. https://www.shopify.com

- Digiday, citing eMarketer on US retail media search advertising of nearly 38 billion dollars, 2026. https://digiday.com

- Gartner, forecast of a 25 percent drop in traditional search volume in 2026.

- McKinsey, "Building the AI advantage: how ADEO is preparing for retail's next wave": Matthieu Grymonprez on full automation, more than 250 AI use cases, and the disillusionment phase, 2026. https://www.mckinsey.com

- Ingka Group (IKEA), Parag Parekh on whether commerce is captured on the agent platform or redirected to the brand, 2026.

- McKinsey and QuantumBlack, "The Automation Curve in Agentic Commerce": the automation curve and optimal delegation, January 2026. https://www.mckinsey.com

- Google retail lead Kapil Dabi, at Shoptalk 2026, on agentic commerce being "not even 2 percent" of digital commerce sales. https://www.shoptalk.com

- YouGov, survey on US trust in AI shopping: 14 percent trust an agent to place an order, 65 percent to compare prices, December 2025. https://today.yougov.com

- McKinsey and QuantumBlack ConsumerWise, "An update on EU consumer sentiment: the uptake of AI shopping tools": 27 European consumer-industry executives, 6 of 27 reporting a profit impact, March 2026. https://www.mckinsey.com

- McKinsey, "Elevating the customer experience: IKEA's agentic AI journey": room design cut from six hours to about 30 minutes and an AI-assisted service channel tied to about 1.3 billion euros a year, June 2026. https://www.mckinsey.com

- Benjamin F. Maier and colleagues, "LLMs Reproduce Human Purchase Intent via Semantic Similarity Elicitation of Likert Ratings," arXiv preprint 2510.08338, October 2025. Not peer reviewed; co-authored with Colgate-Palmolive, which supplied the survey data. https://arxiv.org/abs/2510.08338